Potential Customs and Policies

in Tianjin Pilot Free Trade Zone ("TPFTZ")

By Susan Ju, Partner & Nathan Pan, Manager, PricewaterhouseCoopers

The Shanghai Pilot Free Trade Zone ("SPFTZ") has achieved steady growth since its launch in September 2013. Following the successful footprints of the SPFTZ, a number of new pilot free trade zones ("PFTZ") have been approved and launched in Tianjin, Guangdong and Fujian.

The new PFTZs will try to replicate the success of the SPFTZ and is set to be the frontline in promoting economic growth across China. This summary will serve as a starting point for your reference to the potential policies to be adopted by Customs and CIQ authorities in the TPFTZ.

Overview of TPFTZ

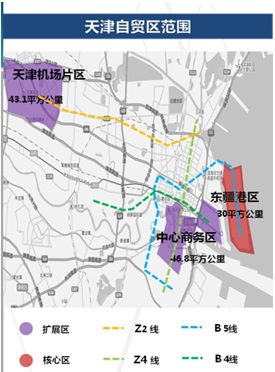

Location:

Location:

Covering 119km2, including:

- Tianjin Port Area (30km2)

- Tianjin Airport Area (43.1km2)

- Binhai CBD Area (46.8 km2)

The coverage area of TPFTZ also includes a number of customs special supervision zones, which. Include the following:

- Tianjin Port Bonded Zone(天津港保税区);

- Tianjin Bonded Logistics Park (天津保税物流园区);

- Tianjin Dongjiang Bonded Port (天津东疆保税港区);

- Tianjin Binhai Integrated Bonded Zone (天津滨海新区综合保税区).

Other areas within the TPFTZ are not subject to customs special supervision measures (e.g. Binhai CBD Area), and so some of the following Customs and CIQ policies may not be applicable.

Highlights of Potential Customs and CIQ policies in TPFTZ

- Open entry in First-line and Effective Control on Second-line

- Open entry in First-line and Effective Control on Second-line

Highlights:

- Enter first and declare later: the imported goods will be allowed to enter the PFTZ prior to customs declaration

- Simple inbound registration: 40 declaration items narrowed to 29 items

- Facilitating the goods movement within the PFTZ: centralized declaration and separate delivery & transportation

- Cooperation between Customs and CIQ: one time declaration, one time inspection and one time release

- Paperless declaration

Function Expansion and Enhancement of New Trade Models

Highlights:

Global bonded repair

Global bonded repair

- Test and repair goods from China and overseas

- Customs supervision with reference to the practice of "bonded manufacturing"

- CIQ adopts simplified supervision measures on "used mechanical and electrical products" entering the PFTZ

Bonded exhibition

- Trade facilitation offered by Customs under "temporary entry and exit " upon "centralized declaration"

- Exhibition outside the PFTZ could be allowed with paid deposit

Cross-border E-Commerce

- Establish CIQ e-system connection with companies

- Personal postal articles tax applied (lower tax rates than on goods)

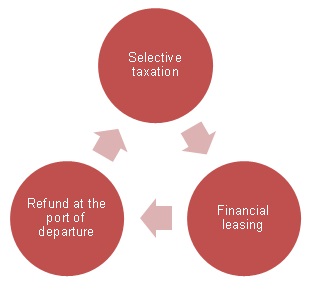

Promote policy implementation

Highlights:

Selective taxation

Selective taxation

- For the goods manufactured or processed in the PFTZ and sold to domestic areas crossing the "second-line", the import duty could be calculated based on corresponding imported raw materials or the actual declaration status of the finished goods for domestic sales.

- Import VAT and consumption taxes (if any) are still applicable based on actual declaration status of the finished goods.

Refund at the port of departure

-The tax refund policy applies to goods declared at certain ports of departure, subject to transit at PFTZ port through waterways to an offshore destination.

Financial leasing

-Enhancement of financial leasing business of aircraft, ship within the PFTZ, etc.

---END---