The Future of RMB

Business Opportunities and Risks

By Hagan Murphy

Almost seven years have passed since the Central Bank of China indicated that it would continue with financial reforms and make the renminbi exchange rate more flexible, thus satisfying major world economies and their leaders who believed that the renminbi was excessively undervalued. Almost seven years later, is the renminbi actually moving towards a freely floating currency, is this the right path to go and will it manage to find a place among the elite global reserve currencies?

Almost seven years have passed since the Central Bank of China indicated that it would continue with financial reforms and make the renminbi exchange rate more flexible, thus satisfying major world economies and their leaders who believed that the renminbi was excessively undervalued. Almost seven years later, is the renminbi actually moving towards a freely floating currency, is this the right path to go and will it manage to find a place among the elite global reserve currencies?

Until 2009, economists agreed that, beside the U.S. dollar and Euro, the third global reserve currency in a multipolar reserve system could either be the Japanese yen, or a kind of incorporated money, called "Asian dollar". With the growing Chinese economy, in line with monetary and economic reforms conducted by the Chinese government, it is seen that the renminbi may become the Asian counterpart currency in the multipolar reserve system.

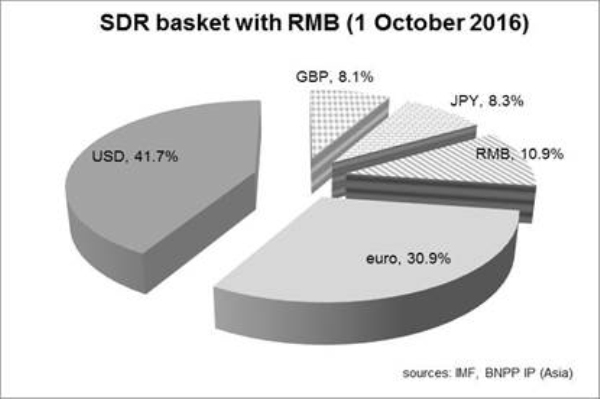

As of October 2016, the renminbi remains included in IMF's artificial currency, namely the Special Drawing Rights, consisting of global reserve currencies such as U.S. dollar, Japanese yen, British pound and euro. This is the first time a currency was added to the basket since the introduction of the euro in 1999. China's central bank has already signed numerous bilateral currency swap agreements with central banks around the world.

The 2016 Triennial Central Bank Survey, conducted by the Bank for International Settlements, showed a significant rise in the importance of renminbi in currency markets. The renminbi became the eighth most actively traded currency, overtaking the Mexican peso. Furthermore, the average daily turnover of the renminbi almost doubled between April 2013 and April 2016, from 120 billion $ to 202 billion $. The USD/CNY currency pair moved up from ninth to sixth place among the most traded currency pairs, with a daily average turnover of 192 billion $. Analysts agree that this trend will persist in future.

The 2016 Triennial Central Bank Survey, conducted by the Bank for International Settlements, showed a significant rise in the importance of renminbi in currency markets. The renminbi became the eighth most actively traded currency, overtaking the Mexican peso. Furthermore, the average daily turnover of the renminbi almost doubled between April 2013 and April 2016, from 120 billion $ to 202 billion $. The USD/CNY currency pair moved up from ninth to sixth place among the most traded currency pairs, with a daily average turnover of 192 billion $. Analysts agree that this trend will persist in future.

The renminbi is also more and more used in international trade agreements, with prospects showing that the Chinese currency may become the second most used currency after the U.S. dollar by 2020. Multinational companies are already issuing bonds denominated in renminbi, showing that the trust in this currency has been rising steadily in recent years. This is an important sign of improving international acceptance of renminbi, otherwise companies would issue bonds denominated in other currencies and hedge their exposure with financial derivatives.

There is no doubt that the renminbi has come a long way since the Chinese government started with reforms in the domestic financial markets, easing capital restrictions on inflows and outflows. But there remain significant hurdles for the Chinese currency to become truly internationally accepted as a global currency.

Although China is taking some necessary steps in liberalizing and regulating its financial markets, they still seem weak and lack regulatory oversight as compared to financial markets of advanced economies. International investors are still not quite impressed with the actions of Xi Jinping's government, which has rolled back the rule of law and independence of key state institutions from government interference.

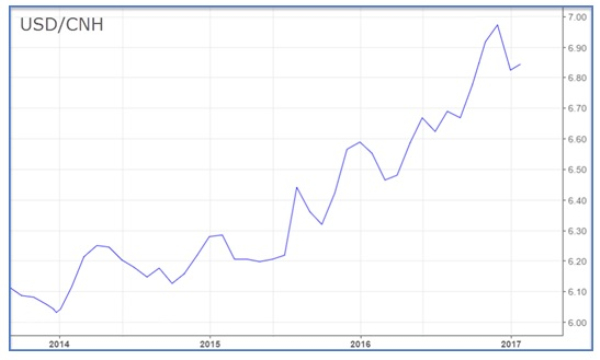

At the World Economic Forum Annual Meeting in Davos, Switzerland, Chinese President Xi Jinping reaffirmed his country's "open door" policy and pledged never to benefit from devaluation of the renminbi. On the other side, the new president of the United States, Donald Trump, has accused China of intentionally devaluing its currency to gain export competitiveness. It is claimed that the renminbi is undervalued by as much as 37% against its purchasing power parity. In reality, China had a tough time battling with downward pressure on its currency and is trying to keep the USD/CNH exchange rate stable.

As exports are falling, China's current-account surplus fell to just 2.1% of GDP in 2016. Economists are predicting the surplus to fall further as exports continue to fall. Also, as China recently shifted to a growth model that encourages higher domestic consumption as opposed to an export-driven model, a weaker renminbi is not quite the path China wants to take. Reports about declining investments and exports have put downward pressure on the Chinese currency which has weakened significantly in recent years from 6.05 to almost 7.00 USD/CNH.

USD/CNH exchange rate, 2014-2017

USD/CNH exchange rate, 2014-2017

While the recent rise of renminbi's importance in global trade and financial markets cannot be denied, forecasts about an absolute dominance of either the renminbi or the U.S. dollar will most likely prove to be wrong. With prospects of overtaking the United States as the largest world economy, China needs inevitably to accelerate the pace of market and state-related reforms, improving the trust of international investors in its currency. Switching to a free-floating currency in the foreign-exchange market heavily dominated by the U.S. dollar would increase the volatility of USD/CNH pair which is not beneficial for China at the moment. A managed float of the renminbi is most likely to stay in the near future.

--- END ---