ANNOUNCEMENT ON SPECIAL TAX INVESTIGATIONS, ADJUSTMENTS AND MUTUAL AGREEMENT PROCEDURES

(PART 2)

By Manuel Torres (Managing Partner of Garrigues China), Diego D’Alma (Principal Associate) & Cynthia Zhou (Tax Associate)

在上一期法律栏目中,我们介绍了国家税务总局发布了《国家税务总局关于发布的公告》,明确了特别纳税调整的风险管理、立案调查调整、复议及相互协商程序相关规则及处理等事项。本期我们将继续这一话题,向大家介绍更多关于《公告》的细节。

上一期我们了解到,《公告》规定了与特别纳税调查调整相关的方法等实施细则,包括:转让定价方法,股权转让的转让定价管理,无形资产的转让定价管理,劳务的转让定价管理,以及一些特殊交易或事项的特别纳税调整方法。其中可比性分析范围扩大了有关资产或服务交易、合同条款、经济环境、商业策略方面的内容。在转让定价方式上,应选择合理的转让定价方法,对企业关联交易进行分析评估。转让定价方法包括可比非受控价格法、再销售价格法、成本加成法、交易净利润法、利润分割法及其他符合独立交易原则的方法。

在关于无形资产方面,其使用权或者所有权的转让包括:无形资产的类别、用途、适用行业、预期收益;无形资产的开发投资、转让条件、独占程度、可替代性、受有关国家法律保护的程度及期限、地理位置、使用年限、研发阶段、维护改良及更新的权利、受让成本和费用、功能风险情况、摊销方法以及其他影响其价值发生实质变动的特殊因素等。

2.COMPARABILITY ANALYSIS AND TRANSFER PRICING METHODS

This section contains a comparative study of Article 15 to Article 22 in Announcement 6 and Chapter 4 of Circular 2. The scope of comparability analysis has been expanded in terms of the following:

a. Asset or service transactions: The character details and risk management etc. of financial assets have been included in Announcement 6.

b. Contract terms: Announcement 6 addresses that analysis of contract terms shall also focus on the ability and conduct of executing the contract by enterprises as well as credibility of contract terms signed by related parties.

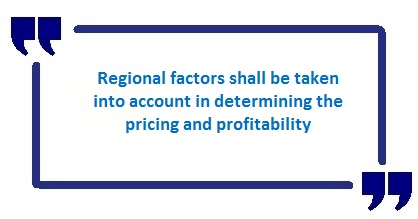

c. Economic environment: Regional factors shall be taken into account in determining the pricing and profitability, for example, cost savings and market premium.

d. Business strategy: Synergy effects have been taken into consideration in Announcement 6.

A number of changes have been made in transfer pricing methods:

e. Comparable uncontrolled price method

i. Following the confirmation of transfer of financial assets between related parties as related party transactions under Announcement 42, the detailed factors to be taken into account for comparable analysis on transfer of financial assets (in particular, equity transfer) have been introduced in Announcement 6.

ii. User right or ownership transfer of intangible assets: The comparative analysis may also consider the factors of geographic location, useful life, development phase, rights of maintenance, improvement and update, costs and expenses of the transferee, functions and risks, amortization method as well as other factors that may have an influence on the fluctuation of prices.

f. Resale price method

i. Comparable analysis on valuable intangible assets for marketing purposes has been suggested by adopting the resale price method, if applicable.

g. Transactional net margin method (“TNMM”)

i. Detailed calculation formulae for profit margin before interest and tax, full cost mark-up, return on assets and Berry ratio are illustrated in Announcement 6.

ii. The applicability of TNMM has been limited to enterprises that do not possess significant intangible assets regarding the ownership transfer or user rights of both tangible and intangible assets. However, Announcement 6 does not specify whether both parties involved in the transaction are subject to limitation of ‘significant intangible assets’. Neither has the said Announcement defined the extent of ‘significant intangible assets’.

h. Profit split method

i. Regional factors, such as cost savings and market premium, have been included in the profit split method.

ii. In the situation that comparable information is difficult to obtain but the consolidated profit (either actual or estimated) can be determined on a reasonable basis, the actual situation and contribution value related factors of income, costs, expenses, assets and number of employees etc. may be considered for the analysis of contribution in value by each related party and distribute the profit accordingly.

i. Other methods that comply with arm’s length principle

i. Other methods may include valuation methods such as cost method, market value method and income method etc. as well as other methods that could reflect the matching principle, i.e. profit shall be taxed in the place wherein economic activities are performed and values are created.

3. INTANGIBLE ASSETS

Article 5 and Article 6 of Announcement 16 in relation to the outbound payments of royalty fees in terms of use of intangible assets of related parties and benefits derived from financing activities of listed companies have been replaced by Article 30, 31 and 33 of Announcement 6. The improvements and developments made in Announcement 6 mainly include the following:

a. Article 30 replaces and supplements Article 5 of Announcement 16 which proposes some approaches in determining the contribution level by each party in the light of the value of intangible assets and the corresponding income distribution including:

i. A comprehensive analysis on the global operating procedures of the group company that the Chinese enterprise belongs to;

ii. Consideration of the contribution value involved in the development and enhancement of value, maintenance, protection, application and promotion (“DEMPAP”); and

iii. Realization method for the value of intangible assets; and

iv. Interaction between intangible assets and functions, risks and assets of other businesses of the group company.

b. Article 30 further stipulates that enterprises that only possess the ownership of intangible assets but do not contribute to the value of intangible assets shall not participate in the income distribution of intangible assets. In addition, enterprises that merely provide funds but do not actually perform related functions and bear related risks during the forming and exploitation process of intangible assets could only obtain reasonable return on the cost of capital.

b. Article 30 further stipulates that enterprises that only possess the ownership of intangible assets but do not contribute to the value of intangible assets shall not participate in the income distribution of intangible assets. In addition, enterprises that merely provide funds but do not actually perform related functions and bear related risks during the forming and exploitation process of intangible assets could only obtain reasonable return on the cost of capital.

c. Article 31 requires that royalty fees received or paid as a result of transfer of user rights of intangible assets between enterprises and their related parties (“Royalty Fees”) shall adjust the amount in accordance with the following situations where special tax adjustment could be made by the tax authority if adjustments are failed to be made by the enterprises themselves:

i. Value of intangible assets has changed fundamentally;

ii. In accordance with usual business practices, an adjustment mechanism of royalty fee shall be in place for comparable transactions between unrelated parties.

iii. Functions performed, risks assumed and assets used by the enterprise and its related parties have changed during the course of exploitation of intangible assets.

iv. The enterprise and its related parties have not been appropriately compensated in the process of continuing DEMPAP of intangible assets.

d. Article 32 addresses the matching principle that Royalty Fees shall be matched with economic benefits generated from intangible assets and flowed into the enterprise or its related parties. If the amount of royalty fee does not match the economic benefits and leads to reduction in the tax payable or taxable income of the enterprise or its related parties, the tax authorities are empowered to make special tax adjustments. Tax authorities could adjust the full amount of deducted expenses of royalty fee, if the said expenses fail to meet the ‘an arm’s length’ principle and fail to bring any economic benefit.

e. Article 31 and 32 of Announcement 6 shift the focus on outbound remittance of royalty fee to both inbound and outbound remittance.

---END---