Financial Accounts of Non-residents

By Manuel Torres (Managing Partner of Garrigues China), Diego D’Alma (Head of Tax Department), Cynthia Zhou (Tax Associate)

2017年5月19日,国家税务总局、财政部、中国人民银行、银监会、证监会以及保监会正式发布2017年第14号公告《非居民金融账户涉税信息尽职调查管理办法》。14号公告的发布标志着由经济合作与发展组织(OECD)所制定的金融账户涉税信息自动交换标准(AEOI标准)在中国正式实施。新办法实施后有很多细节值得我们注意。首先,需要报送信息的个人和机构包括非中国税收居民的个人、企业和其他机构,消极非金融机构以及它们的非中国税收居民控制人的信息也需要上报。某些国际组织、政府机构、央行、金融机构以及上市公司是不需要被上报信息的。需要报送的财务、税务、账户信息有:账户持有人的姓名/机构名、税收居民国(地区)、居民国(地区)纳税人识别号、出生地、出生日期(如果适用)、账号、账户公历年度末余额以及账户公历年度内的收入等。

2017年5月19日,国家税务总局、财政部、中国人民银行、银监会、证监会以及保监会正式发布2017年第14号公告《非居民金融账户涉税信息尽职调查管理办法》。14号公告的发布标志着由经济合作与发展组织(OECD)所制定的金融账户涉税信息自动交换标准(AEOI标准)在中国正式实施。新办法实施后有很多细节值得我们注意。首先,需要报送信息的个人和机构包括非中国税收居民的个人、企业和其他机构,消极非金融机构以及它们的非中国税收居民控制人的信息也需要上报。某些国际组织、政府机构、央行、金融机构以及上市公司是不需要被上报信息的。需要报送的财务、税务、账户信息有:账户持有人的姓名/机构名、税收居民国(地区)、居民国(地区)纳税人识别号、出生地、出生日期(如果适用)、账号、账户公历年度末余额以及账户公历年度内的收入等。

我们可以看到,根据新的管理办法,非居民金融账户涉税信息调查范围很全面,持有离岸金融账户、金融资产或从中取得收入的中国税收居民应尽快从中国和外国税务角度重新评估或分析其总体税务合规状况,以尽量减少税务风险。对于希望在中国金融机构开立账户的非居民个人,请准备在开立帐户过程中提供更详细的信息,包括其税收居民国提供的纳税人识别号(TIN)。

本《管理办法》中所指“金融机构”包括存款机构、托管机构、投资机构、特定的保险机构及其分支机构,如商业银行,农村信用社和政策性银行,证券公司,期货公司,证券投资基金管理公司,私募基金管理公司,从事私募基金管理业务的合伙企业,开展有现金价值的保险或年金业务的保险公司,保险资产管理公司,信托公司等。“金融账户”包括存款账户,托管账户,投资账户,合伙权益,信托受益权以及具有现金价值的保险合同或年金合同。“金融资产”包括证券,合伙权益,大宗商品,掉期,保险合同,年金合同或期货,远期合约或期权等上述资产的权益。

关于需要报送信息的人是指除中国税收居民以外的个人,企业和其他组织,不包括政府机构,国际组织,中央银行,金融机构或上市公司及其关联公司。中国税收居民是指按照中国税法规定为税收居民的单位或个人。企业的“控制人”定义为直接或间接拥有超过 25%公司股权或者表决权的个人;通过人事、财务等其他方式对公司进行控制的个人以及公司高级管理人员。

“账户持有人”包括由金融机构登记或确认为账户的所有者的个人或机构,但不包括代理人,名义持有人或授权签字人。 同时,现金价值保险合同或年金合同的“账户持有人”可以是有权获得现金价值或更改合同受益人的任何个人或机构,也可以是根据合同条款对支付款项拥有既得权利的个人或者机构。

此外,“消极非金融机构”包括主要获得消极投资收益(不属于公历年度积极经营活动)的非金融企业; 资产主要是能够产生消极投资收益的金融资产的非金融企业; 不实施 AEOI 标准的国家(地区)税收居民的投资机构。同时要注意,一些非金融机构不被认为是消极非金融机构,例如,上市公司及其附属企业;履行公共服务职能的政府部门或者机构;仅为了持有非金融机构股权或者向其提供融资和服务而设立的控股公司;成立时间不足二十四个月,尚未开展业务的企业;正在清算或重组的企业;集团内的财务中心和非营利组织。

On May 19th, 2017, the State Administration of Taxation (“SAT”), the Ministry of Finance, the People's Bank of China, the China Banking Regulatory Commission, the China Securities Regulatory Commission, as well as the China Insurance Regulatory Commission issued an announcement on the Administrative Measures of Tax Information Due Diligence for Financial Accounts of Non-residents (“Announcement 14”) to implement the information exchange (“IE”) of financial accounts between China and other participated countries or jurisdictions . The following sections provide a nutshell of Announcement 14 and the potential tax impact on non-residents who have financial accounts in China -

On May 19th, 2017, the State Administration of Taxation (“SAT”), the Ministry of Finance, the People's Bank of China, the China Banking Regulatory Commission, the China Securities Regulatory Commission, as well as the China Insurance Regulatory Commission issued an announcement on the Administrative Measures of Tax Information Due Diligence for Financial Accounts of Non-residents (“Announcement 14”) to implement the information exchange (“IE”) of financial accounts between China and other participated countries or jurisdictions . The following sections provide a nutshell of Announcement 14 and the potential tax impact on non-residents who have financial accounts in China -

1. Purpose of Announcement 14

Announcement 14 provides legal basis and guidance for Chinese financial institutions to conduct tax information due diligence (“TDD”) on financial accounts of non-residents. It aims to improve the transparency of tax information by enhancing the cooperation among tax authorities in different countries or jurisdictions and oppose tax avoidances by sharing the information of non-residents’ offshore accounts. In order to achieve this aim, Announcement 14 specifies the target (i.e. non-resident explained in section 2), the assessor (i.e. financial institutions explained in section 3), the scope (i.e. financial accounts explained in section 4) and the implementation (i.e. TDD and reporting explained in section 5).

2. Definition and assessment of non-resident

2. Definition and assessment of non-resident

According to Announcement 14, assessment of the resident status of the account holder is the key process of the TDD, which directly determines whether Announcement 14 would have an impact on the account holder. A non-resident refers to an individual or an enterprise (including other organizations) that is not a Chinese tax resident .

However, the abovementioned non-resident does not include government authorities, international organizations, central banks, financial institutions, listed companies or affiliates of listed companies.

Financial institutions, as the assessor of non-resident, would apply a ‘Factor Test’ by referring to one or more than one of the criteria listed below for identification of non-residents on their own discretion:

- The account holder has an overseas identity document(s) (e.g. passport);

- The account holder has an overseas residential address or mailing address;

- The account holder has an overseas telephone number and does not have any Chinese telephone number;

- There are regular instructions of transfers from the inbound account (excluding deposit accounts) to overseas accounts;

- The account agent or authorized signatory has an overseas address; and

- The account only has an overseas notification address.

Based on the above, individuals and institutions could perform self-review on the account information provided to financial institutions so as to assess whether they have fallen or will fall into the scope of non-resident under Announcement 14.

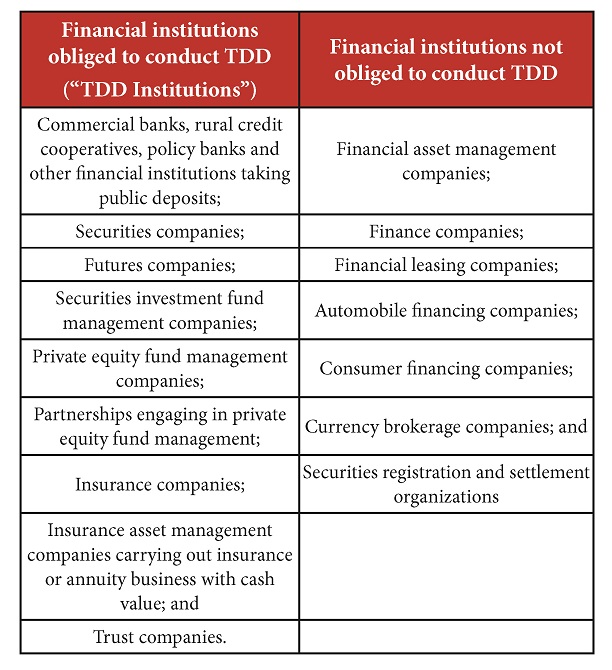

3. Financial institutions for TDDs

With reference to Announcement 14, not all financial institutions are obliged to conduct TDD. The following table demonstrates the financial institutions that are obliged to conduct a TDD, and those that are not.

Hence, a non-resident that has a financial account in TDD Institutions would be monitored and reported if the financial account met other specified requirements explained in the below sections.

Hence, a non-resident that has a financial account in TDD Institutions would be monitored and reported if the financial account met other specified requirements explained in the below sections.

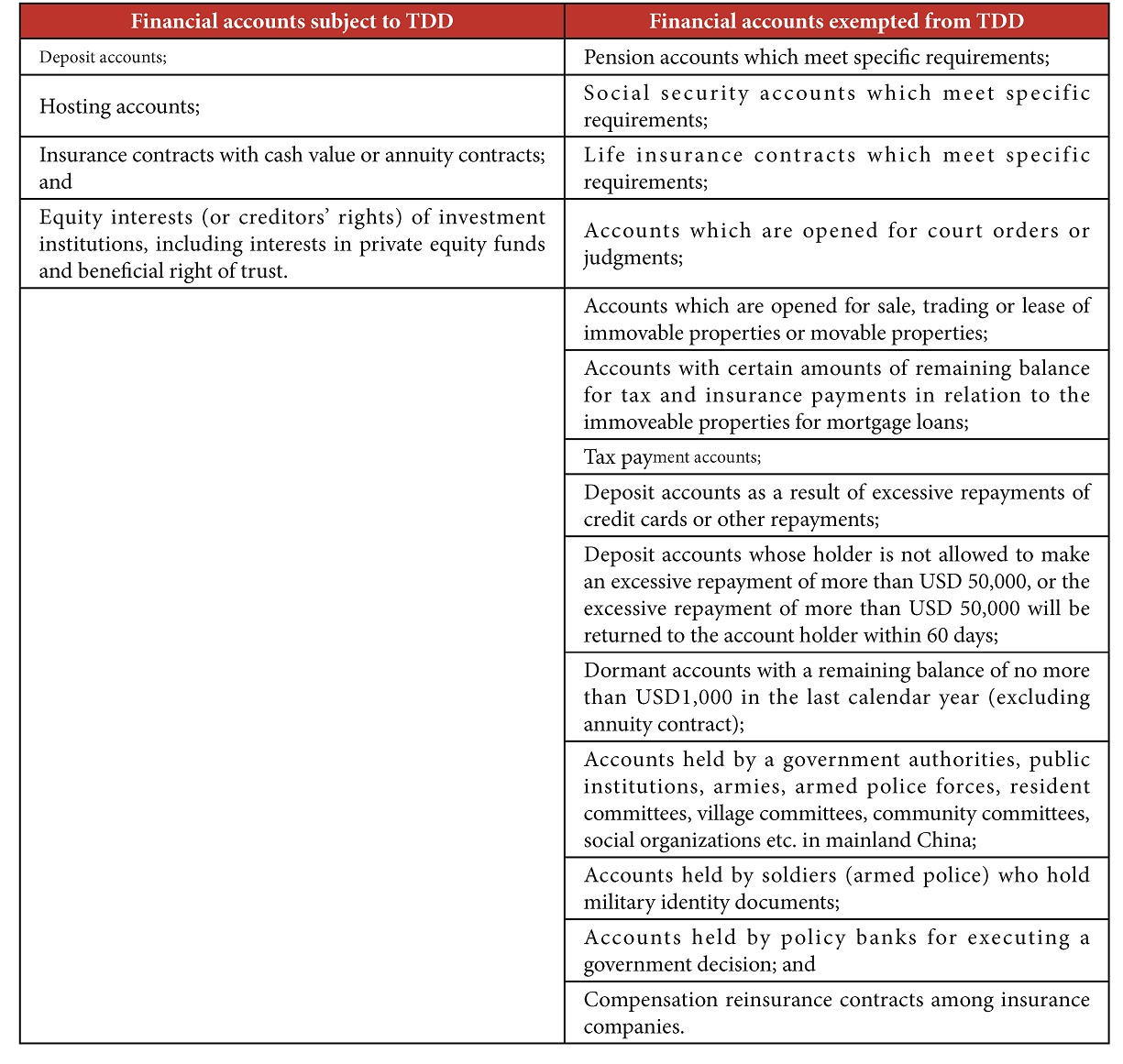

4. Financial accounts for TDD

Announcement 14 specifies that individual’s financial accounts will be subject to TDD regardless of the account balance, whereas financial accounts of institutions have to show a balance exceeding USD 250,000 to be subject to conduct TDD. In the case that a non-resident directly (or indirectly) owns (or controls) several financial accounts in the same TDD Institution (including the affiliates of the TDD Institution), the account balance shall be the total value of these accounts.

The following table provides the types of financial accounts that are subject to or are exempted from TDD:

5. TDD and reporting

Procedures of TDD depend on the types of financial accounts (i.e. individual’s financial accounts or institution’s financial accounts), as well as the opening date of financial accounts. Financial accounts have been further divided into 4 groups, including new individual’s financial accounts, existing individual’s financial accounts, new institution’s financial accounts and existing institution’s financial accounts.

Individual’s financial accounts

Individual’s financial accounts

- New individual’s financial accounts

A financial account opened on or after July 1st, 2017, may be regarded as a new financial account. In case that the account holder has already had an existing financial account in the same financial institution but opens a new financial account on or after July 1st, 2017, the later account would not be treated as a new financial account.

Holders of individual’s financial accounts shall sign a statement regarding their tax resident status before opening individual accounts since July 1st, 2017. The TDD Institutions will check the reasonableness of the statements. If a statement is suspected as unreasonable, the TDD Institution may ask the individual to submit additional supporting documents to further verify the authenticity of the statements or to give explanations. In case that the additional supporting documents are still considered as unreasonable, the TDD Institution would deny the application for opening a new account.

When the new individual’s financial account is ready to use, it shall be regarded as an existing individual’s financial account. The TDD and reporting rules for existing individual’s financial accounts will be applied.

- Existing individual’s financial accounts

For existing individual’s financial accounts (“EIFAs”), the requirements for TDD differ based on whether the account is a high-net-worth account6 or a low-net-worth account . The TDD institutions would further assess the EIFAs by adopting the following methods:

(i) Searching the electronic records in the existing information system or assessing the available information of an existing account holder by applying the ‘Factor Test’ as mentioned in section 2). If holders of the EIFAs are assessed as non-residents, information of their financial accounts will be reported to the Chinese tax authorities. If TDD Institutions cannot assess the resident status of an account holder based on the existing information, the account holder will be required to provide a statement regarding his/her tax resident status. A failure in providing such documents would be considered as a non-resident; and

(ii) Investigating the client manager (for high-net-worth accounts only).

The first TDD for existing non-resident individual accounts with high net worth and low net worth shall be finished by December 31st, 2017 and December 31st, 2018 respectively. After determining the non-resident individual accounts for reporting to the Chinese tax authorities, the first IE will take place in September 2018. The account balances of EIFAs with low net worth that exceed USD 1,000,000 at the end of any calendar year after June 30th, 2017, shall be treated as high-net-worth accounts. The corresponding ongoing TDDs shall be finished by December 31st of the following year. Accordingly, the second IE will be held in September 2019.

Institution’s financial accounts

Institution’s financial accounts

TDD Institutions perform TDD procedures by assessing the resident status of the account holder, determining whether the account holder is a passive non-financial institution , as well as examining the control status of the account holder.

- New institution’s financial accounts

New institution accounts, which are opened on or after July 1st, 2017, are classified into 6 groups by applying different TDD procedures accordingly.

- Existing institution’s financial accounts

- Existing institution’s financial accounts

Regarding existing institution’s financial accounts, TDD Institutions will conduct assessments to specify the resident status of the account holder, whether the account holder is a passive non-financial institution and whether the account is controlled by a non-resident in order to determine the TDD and reporting policies.

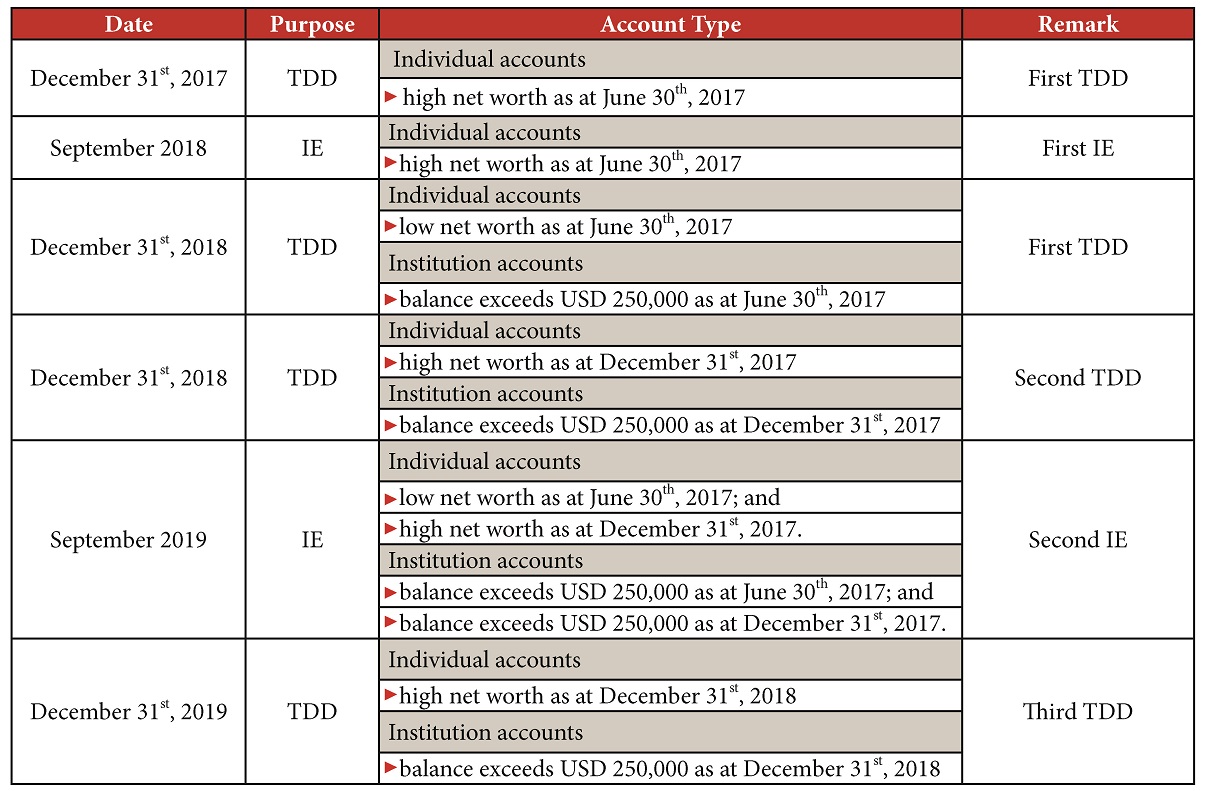

6. Conclusions

6. Conclusions

In summary, the below timetable demonstrates the deadlines for different types of financial accounts in correspondence with the first time and ongoing TDDs and IEs:

Financial accounts of non-PRC tax residents, which have satisfied certain conditions, will be reported by Chinese tax authorities to the tax authority located in the home country of the individual or an institution which participates in the IE. On one hand, PRC Individual Income Tax (“IIT”) Law is applicable to the assessment of non-PRC tax resident for individuals, which requires that non-Chinese individuals are subject to Chinese IIT either (a) when they qualify as a tax resident in China, which will depend on the number of staying days in China or (b) when they derive income from sources inside China. On the other hand, PRC Enterprise Income Tax (“EIT”) Law shall be applied in assessing the non-PRC tax resident for enterprises, which are subject to the registered location and the management location of the enterprise. It is recommended that account holders (or controllers) of financial accounts, which are affected by Announcement 14, shall pay special attention on the global tax compliance status to avoid tax disputes.

Furthermore, the account information of a PRC tax resident that holds overseas financial accounts opened in a country or a jurisdiction engaged in the IE will be reported to Chinese tax authorities, provided that it meets the requirements of IE in the respective country or jurisdiction. According to PRC EIT and IIT Laws, worldwide income of a PRC tax resident shall be taxable in China. Chinese tax authorities could check if there is any missing tax filing or underpaid tax based on tax information exchanged by tax authorities in other countries or jurisdictions. Any non-compliance tax issue would be subject to higher tax risks due to the increase in transparency.

---END---