Increased Certainty in the Assessment of Beneficiary Owner

Opportunity for Foreign Investors?

2018年2月3日,国家税务总局发布了《关于税收协定中“受益所有人”有关问题的公告》,简称9号公告。9号公告保留、延续了国税函601号文件和国家税务总局公告第30号文件中的部分规定,并对原文件中的受益所有人的判断标准、安全港规则以及税收居民身份证明的要求等进行了修订,整体替代了601号文和30号文,使得我国的受益所有人的判定规则得到进一步完善。特别值得一提的是,9号公告的解读提供了很多图示和指南,从而大大增加了9号公告在实际执行中的确定性和可操作性,明确了“受益所有人”身份判定的适用范围。

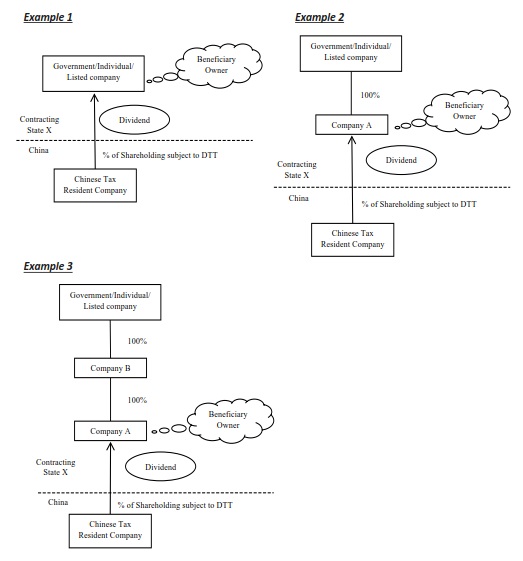

据公告显示,申请人从中国取得的所得为股息时,申请人虽不符合“受益所有人”条件,但直接或间接持有申请人100%股份的人符合“受益所有人”条件,并且属于以下两种情形之一的,应认为申请人具有“受益所有人”身份:(一)上述符合“受益所有人”条件的人为申请人所属居民国(地区)居民;(二)上述符合“受益所有人”条件的人虽不为申请人所属居民国(地区)居民,但该人和间接持有股份情形下的中间层均为符合条件的人。同时,下列申请人从中国取得的所得为股息时,可不根据本公告第二条规定的因素进行综合分析,直接判定申请人具有“受益所有人”身份:(一)缔约对方政府;(二)缔约对方居民且在缔约对方上市的公司;(三)缔约对方居民个人;(四)申请人被第(一)至(三)项中的一人或多人直接或间接持有100%股份,且间接持有股份情形下的中间层为中国居民或缔约对方居民。

9 号公告表示“受益所有人”身份判定适用于股息、利息和特许权使用费条款。换言之,“受益所有人”身份判定不包括财产转让所得。这就避免了原先 601 号文模糊规定可能导致的实操中的歧义和执法不一。

9 号公告还放宽了享受税收协定待遇的范围:首先扩大了安全港的范围,其次在子公司不满足“受益所有人”测试时,允许穿透到母公司,依据母公司的经济实质来判定,即使母公司与子公司不在同一国家。

公告也对部分不利因素做出了修改。第一,9号公告对 601 号文的第一项不利因素(即对其取得的所得在一定时限内有一定比例的支付义务)进行了两方面的修改:将支付比例从原先的 60%降低到 50%,并提出虽未约定义务但已形成支付事实的也构成不利因素。

基于 601 号文中的第二至第四项不利因素均与实质性经营活动相关,因此,9 号公告基本上将这三项不利因素整合为一项不利因素,进一步明确了实质性经营活动的内容和判定,以及进一步将“从事的其他经营活动不够显著”,判定为不构成实质性经营活动。这一规定与投资管理公司尤其相关。

整体来看,9号公告体现了税务总局对主要目的测试条款的应用,可以说是中国税务机关在税收协定的解释和执行方面与国际接轨跨出的一大步,将受到非居民纳税人欢迎。

The State Administration of Taxation (“SAT”) issued Announcement on Issues Concerning ‘Beneficiary Owners’ in Tax Treaties, SAT [2018] No. 9, effective from April 1st, 2018 (“Announcement 9”), which replaced the former Guo Shui Han [2009] No. 601 and SAT [2012] No. 30 by revising the ‘adverse factors’ for assessment of beneficiary owners (“Assessment”), widening the scope of ‘safe harbor’ rules, and allowing ‘look through’ for the Assessment with certain conditions, etc. Moreover, SAT has issued an interpretation to Announcement 9 for further clarifications (“Interpretation”).

Tax Benefits of Beneficiary Owners

Under the prevailing Chinese Enterprise Income Tax (“EIT”) rules, a non-tax resident company that either not having an establishment in China but deriving income sourced from China or having an establishment in China but the income derived not being related to the establishment in China, is subject to an EIT rate of 10% on the China-sourced income, including dividends, royalties and interest (“Income”). However, the Double Taxation Treaties between China and some certain contracting states (“DTTs”) provide reduced EIT rates in articles of dividends, interest and royalties for beneficiary owners.

Following the introduction of SAT Announcement [2015] No. 60 , which abolishes the application and approval procedures for treaty benefits and implements the reporting obligations of non-resident taxpayers or their withholding agents, the law requires non-resident taxpayers or their withholding agents to assess the eligibility of treaty benefits on their own and to voluntarily report the need for treaty benefits to the competent tax authority for future tax administration purpose.

Following the introduction of SAT Announcement [2015] No. 60 , which abolishes the application and approval procedures for treaty benefits and implements the reporting obligations of non-resident taxpayers or their withholding agents, the law requires non-resident taxpayers or their withholding agents to assess the eligibility of treaty benefits on their own and to voluntarily report the need for treaty benefits to the competent tax authority for future tax administration purpose.

The clarity and certainty in determining the beneficiary owner has been a challenging area for foreign investors and the withholding agent of foreign investors for many years. On one hand, Announcement 9 allows the beneficiary owners to enjoy tax treaty benefits with more certainty and promotes the business environment. On the other hand, it clarifies adverse factors which undermine the Assessment and therefore prevents the abuse of the DTTs. The said beneficiary owner is the non-resident taxpayer who has the voluntary reporting obligations for treaty benefits and will be hereinafter referred to as “Self-assessor”.

“Adverse Factors” Assessment

The ‘adverse factors’ Assessment has been reduced from ‘7 adverse factors’ Assessment in Guo Shui Han [2009] No. 601 to ‘5 adverse factors’ Assessment in Announcement 9. Nevertheless, there has been no fundamental change in the Assessment, which continues to address the significance of ‘substantive business activities’. In general, the following five factors are regarded as adverse factors to the Assessment:

- The Self-assessor is obliged to pay more than 50% of the Income to a resident in a third country (region) within 12 months upon receiving the Income (“Factor 1”);

- The Self-assessor does not have substantive business activities (“Factor 2”). Substantive business activities include substantive manufacturing, distribution, management (such as management in investment holdings), etc. The level of substantive business activities are assessed in accordance with the actual functions performed and the risk assumed; and

- The other contracting state (region) does not levy tax or grant tax exemption on the Income or apply an extremely low effective tax rate (“Factor 3”).

- Besides the loan agreement based on which the interest is generated and paid, there are other similar loans or deposit contracts in terms of amount, interest rate and execution date etc. between the Self-assessor (as debtor) and its creditor (“Factor 4”); and

- Besides the contract for the transfer of user rights in respect of copyright, patent or technology (“Royalty Contract”) based on which the royalties are generated and paid, there are other Royalty Contracts in respect of the right to use or the ownership of copyright, patent or technology between the Self-assessor (as licensee) and licensor (“Factor 5”).

Based on the above, the table below summarizes the applicability of each adverse factor for different types of Income.

Expanded Scope of ‘Safe Harbor’ Rules for Dividends

Expanded Scope of ‘Safe Harbor’ Rules for Dividends

Guo Shui Han [2009] No. 601 and SAT [2012] No. 3 only allowed the Self-assessor to be eligible for beneficiary owner, provided that the Self-assessor receives dividends from a Chinese enterprise and is a listed company or 100% held by a listed company directly or indirectly in the same contracting state of the Self-assessor. In comparison, the prevailing ‘safe harbor’ rules have been expanded from listed companies in the other contracting states to governments and individual residents of the other contracting states.

Exceptional Rules of Assessment for Self-assessors Receiving Dividends

Exceptional Rules of Assessment for Self-assessors Receiving Dividends

Announcement 9 has further stipulated exceptional rules of Assessment for Self-assessors who receive dividends but cannot be assessed as beneficiary owners through the ‘adverse factors’ Assessment (“‘Adverse Factors’ Self-assessor”). The exceptional rules allow the ‘Adverse Factors’ Self-assessor to be recognized as a beneficiary owner and enjoy the DTT benefits of lower tax rates, provided that the shareholder of the ‘Adverse Factors’ Self-assessor, who directly or indirect holds 100% of shares of the ‘Adverse Factors’ Self-assessor, is recognized as a beneficiary owner (“Qualified Shareholder”) and meets one of the two conditions concurrently:

- The Qualified Shareholder is a resident in the same contracting state as the ‘Adverse Factors’ Self-assessor (“Condition I”); or

- The Qualified Shareholders and the intermediate shareholders are all eligible for the same or more preferential DTT benefits compared to the ‘Adverse Factors’ Self-assessor’s (“Condition II”).

Other rules stipulated in Announcement 9

Other rules stipulated in Announcement 9

In addition to the above, Announcement 9 has also included the following aspects in relation to the Assessment:

- Agent or appointed payee, who receives Income on behalf of the beneficiary owner, will not be assessed as beneficiary owner nor has an impact on the Assessment in any case;

- Examples of supporting documents for the Assessment;

- Reference to SAT Announcement [2015] No. 60 for the procedures of enjoying DTT benefits;

- Requirement for competent tax authorities for the future tax administration of anti-tax avoidance; and

- Applicability of Announcement 9 to DTT between China and Hong Kong as well as DTT between China and Macau.

Commentary on Announcement 9

Commentary on Announcement 9

Announcement 9 and the Interpretation have increased the certainty in the Assessment for the concept of ‘substantive business activities’, widening the scope of ‘safe harbor’ rules and providing exceptional rules for ‘Adverse Factors’ Self-assessors to be recognized as beneficiary owners through Qualified Shareholders. It is useful to Self-assessors for evidencing the eligibility of beneficiary owners to the competent tax authorities and may reduce the discrepancy of Assessment in local practices.

Understanding of beneficiary owner in international taxation generally concentrates on the degree of control over the Income. In comparison, the ‘adverse factors’ Assessment in Announcement 9 has more stringent requirements, where the degree of control is one of the factors among others. The ‘substantive business activities’ in the Assessment is an additional Chinese interpretation for the concept of beneficiary owner.

Furthermore, Announcement 9 requires the competent tax authorities to apply for either the investigation procedures of general anti-tax avoidance rules under the domestic tax rules or the primary purpose test in the DTTS for the Assessment, if they identify any case of DTT abuse. Applications of the general anti-tax avoidance rules and the primary purpose test are questioned due to lack of guidance on when and how can these be applied to or initiated on the Assessment.