China’s Solar PV Power

By Glenda Jarvis

中国太阳能光伏发电

中国太阳能光伏发电

可再生能源的主要来源之一是太阳能资源。虽然光伏(PV)是世界上广泛使用的太阳能技术,它通过使用硅制造的材料将太阳光转化为电能。除此之外,太阳能光伏发电的好处是它方便,清洁,高效以及安全。人们对于环境污染的担忧和全球能源危机的意识都显示了如今使用太阳能光伏发电的重要性。

太阳能光伏产业的发展

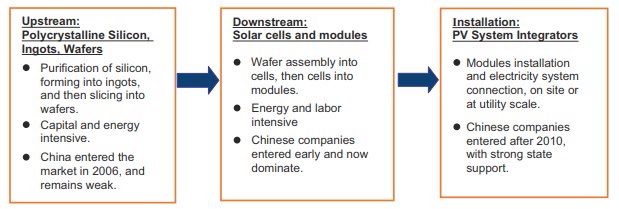

太阳能光伏产业涉及几个阶段:(1)第一阶段是净化硅,被转化为硅锭,然后将其成型转化为薄晶圆,然后将硅锭切成薄片; (2)切割的薄晶片将会根据喜好,打造太阳能电池的形状和尺寸; (3)为了形成太阳能电池组件,太阳能电池会被连接并层压; (4)光伏系统是在太阳能组件组装完成后再与电气元件组合而成; (5)欧洲国家对光伏发电的需求急剧增加,特别是2004年德国的激增需求。中国的光伏生产的增长导致从多晶硅,电池到晶圆和模块的大规模生产,促进了国内供应链。

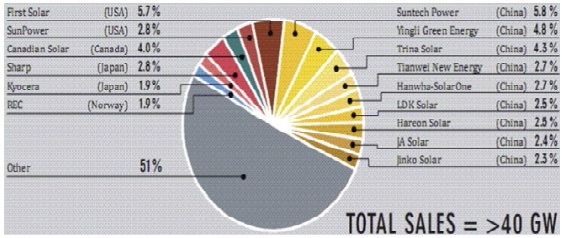

根据图表,全球有十五家太阳能光伏组件制造商,其中九家是中国所有,占全球30%的份额。除此之外,随着太阳能电池质量的提高,中国的太阳能光伏技术生产也在不断进步。此外,如图所示,在转换效率方面,中国的公司也是领先者。

市场进展

中国太阳能市场化正处于关键阶段,必须运用到中国太阳能市场的若干有效资源。例如通过招标购买新建的电力项目和公用事业规模的太阳能项目。地方政府能通过法规,在当地太阳能市场上进行合理的竞争。中国也不是唯一的太阳能组件生产商。

根据NEA的调查,中国计划在2018年前实现13.9GW的公用事业规模项目。 AECEA的2018年报告显示,2016 - 2020年(第13个五年计划)可能不会放缓。

AECEA表示这些激进措施不仅会减缓2018年的需求,还会持续到“十三五”规划(2016-2020)结束。在2017年,中国已经部署了34GW公用事业规模计划,因为光伏的影响不容小觑。

太阳能光伏发电在中国的意义

在中国,太阳能光伏发电的影响常见于上表所示的五个领域中。表格也显示了例如充电和灯光等商业商品。

政策

光伏发电有许多的激励措施,例如

(1)正确预估需求,以达到最好的经济效益,降低价格

(2)不懈努力达到预期前景。不断投资太阳能生产

(3)清晰政策以及不断更新。通过个人评估风险以及作出投资决定。

前景

直至2018年,此图标分析了对中国光伏政策发展的修正。对总体部署有着重大影响。此外,2016年至2020年(第十三个五年计划)的观点仅针对40GW至45GW的年度部署规模,以及基于AECEA报告的30GW至35GW,正如上图所示。住宅市场正在逐步成为新兴市场,在2018年底已经达到5GW的光伏装置。

One of the major sources of renewable energy is the solar power resource. Photovoltaic (PV) is widely used solar power technology in the world, which converts sun’s rays into electricity by using silicon made material. Additionally, benefits of Solar PV power generation are that it is convenient, easy to clean, highly effective and safe. Besides these, there is a concern over environmental pollution and global energy crisis that has rendered solar PV power important.

Progress in Solar PV Industry

There are several stages that are involved in the solar PV industry, so let’s look at them: (1) first stage is cleansing silicon that is converted into ingots and then shaping it up, and converting it into thin wafers, which are then sliced; (2) shapes and dimensions are designed according to the blades that cut the thin wafers to produce solar cells; (3) in order to form solar module, solar cells are connected and laminated; (4) the PV system is made when the solar module is assembled and combined with electrical components; (5) demand for PV has drastically increased in European countries, particularly in Germany. In the year 2004, there has been a drastic growth in China’s PV production that has led to massive solar production from poly-silicon cells to wafers and modules. All of this has caused a rise in the domestic supply chain.

Expansion

Expansion

As per the chart, there are top fifteen manufacturers of solar PV module in the world, out of which nine are owned by Chinese companies, thus accounting for a share of 30%. Besides this, China is progressing in its solar PV technology production along with improvement in the solar cell quality. Moreover, there is a rapid progress in the leading companies when it comes to effective conversion as seen in the figure.

Market Progress

Market Progress

Marketing of China’s solar production is poised at a crucial stage wherein necessary implementation of several resources that are available in China’s solar market is required in terms of allocation. Thus, a bidding process is used to buy power projects that are newly built and also utility-scale solar projects. It further instructs local governments to pass regulations and proceed forward in the local solar market to encourage reasonable competition. Although a country like China is not the only producer of solar module, it is investing huge amounts on solar PV equipment that adds to inverters, solar experts and workers. The notice issued in the starting of 2018 has left its influence on worldwide solar industry that globally costs would be more than the prices of module.

According to NEA guidance, China had positioned 13.9GW placement of utility-scale programs by 2018. Besides this, the 2018 notice has further highlighted the utility-scale by targeting and getting abolished after instructing all provincial districts to execute a ban on every unit, which fits the 2018 mechanism as shown in the table. The report by AECEA released in 2018 states that there might not be a slowdown within the time-frame between 2016 and 2020(13th Five Year Structure).

AECEA said that this drastic measure would not only slow down demand in 2018, but carry through to the end of the 13th Five-Year-Plan (2016-2020). During the year 2017, China has deployed 34GW utility scale plans as the effect would not be underestimating on photovoltaic deployments.

Implication of Solar PV Power in China

In China, concentration of solar PV power is seen in five sectors as the table above shows: there is an off-grid solar PV in rural and distant areas; and further it shows that telecommunications, transportation and other industries all come under off-grid solar. Moreover, the table shows commercial products along with chargers and lights wherein on-grid covers BIPV (building solar PV) that is made of integrated solar PV by BAPV (Building Attached PV), is big-scale (also known as utility scale) version of solar PV.

In China, concentration of solar PV power is seen in five sectors as the table above shows: there is an off-grid solar PV in rural and distant areas; and further it shows that telecommunications, transportation and other industries all come under off-grid solar. Moreover, the table shows commercial products along with chargers and lights wherein on-grid covers BIPV (building solar PV) that is made of integrated solar PV by BAPV (Building Attached PV), is big-scale (also known as utility scale) version of solar PV.

Policy

Successful incentives of PV group are as follows:

(1) The predictable demand is driven adequately. Sufficient margin is required for incentives to influence basic market makeover in order to move solar PV technology prices to lower levels;

(2) Constant and foreseeable critical view is imperative to ensure that policy stability remains progressive. In order to have continuous investments in the solar manufacturing and development industry, the policy maker needs to foresee the industry and its development period.

(3) Remaining clear and updated is a requirement that there should be clear definition on policies that are addressed simply and allow a comprehensive range of market leaders by adding individuals to simply evaluate risks and make decisions over investment.

Future Prospects

By 2018 and beyond, it has analyzed the unexpected and thoughtful modifications to PV deployment in China, which is measuring a major impact on total deployments. Further, perspective of 2016 to 2020 (13th Five Year Program) has targeted only yearly deployments scale of 40GW to 45GW that is based on AECEA report as shown in the above chart. Moreover, divisions that are intact up till now are rapidly excelling in the residential market, which shows that PV installation has moved to 5GW by the end of 2018.