The Reform to Facilitate the De-registration of Enterprises

Tax De-registration Procedures are refined continually

By Kelvin Lee, PWC

In recent years, in order to optimize the business environment and promote high-quality economic development, the Chinese government has been putting forward a series of initiatives for the reform of “Streamlined Administration, Delegated Powers, Improved Regulations and Services” to accelerate the transformation of government functions and to vitalise the market. Since the reform of “Streamlined Administration, Delegated Powers, Improved Regulations and Services”, the business registration procedure of enterprises has been streamlined, but the problems in tax de-registration have been increasingly prominent.

In recent years, in order to optimize the business environment and promote high-quality economic development, the Chinese government has been putting forward a series of initiatives for the reform of “Streamlined Administration, Delegated Powers, Improved Regulations and Services” to accelerate the transformation of government functions and to vitalise the market. Since the reform of “Streamlined Administration, Delegated Powers, Improved Regulations and Services”, the business registration procedure of enterprises has been streamlined, but the problems in tax de-registration have been increasingly prominent.

To deepen the reform of “Streamlined Administration, Delegated Powers, Improved Regulations and Services”, response to the concerns of market players and solve the problems in tax de-registration, on 18th of September, 2018, the State Taxation Administration (hereinafter referred to as “STA”) issued the Notice of the STA on Further Refining the Tax De-registration Procedures of Enterprises (Shuizongfa [2018] No. 149, hereinafter referred to as “Circular No. 149”), introducing a series of measures to facilitate taxpayers in tax de-registration effective from 1st of October, 2018.

Since Circular No. 149 took effect, the efficiency in tax de-registration has been significantly improved. To further optimize the tax business environment, on 9th of May, 2019, the STA issued the Notice of the STA on Deepening the Reform of “Streamlined Administration, Delegated Powers, Improved Regulation and Services” to Further Refine the Tax De-registration Procedures of Enterprises (Shuizongfa [2019] No. 64, hereinafter referred to as “Circular No. 64”), proposing additional measures to refine the tax de-registration procedures for taxpayers.

In this article, we will introduce the specific measures that facilitate taxpayers in the tax de-registration process under Circular No. 149 and Circular No. 64, analyse its impact on taxpayers, as well as share with you our observations.

近年来,为优化营商环境,推动经济高质量发展,中国政府出台了一系列“放管服”改革措施,加快政府职能转变,激发市场主体活力。随着“放管服”改革的推进,企业注册越来越方便,但是企业“注销难”的问题却日益突出。为贯彻落实深化“放管服”改革要求,回应市场主体关切,破解企业注销难题,国家税务总局(以下简称“国税总局”)于2018年9月18日发布《关于进一步优化办理企业税务注销程序的通知》(税总发[2018]149号,以下简称“149号”),自2018年10月1日起实行了一系列便利纳税人办理税务注销的措施。149号文施行以来,企业办理税务注销效率显著提高。为进一步优化税收营商环境,国税总局于2019年5月9日发布《关于深化“放管服”改革 更大力度推进优化税务注销办理程序工作的通知》(税总发[2019]64号,以下简称“64号”),在149号文的基础上进一步推出优化税务注销流程的多项举措,为纳税人办理注销再添便利。

在本文中,我们将介绍149号文和64号文实行的便利纳税人办理税务注销程序的具体措施,分析其对纳税人的影响并分享我们的观察。

In detail

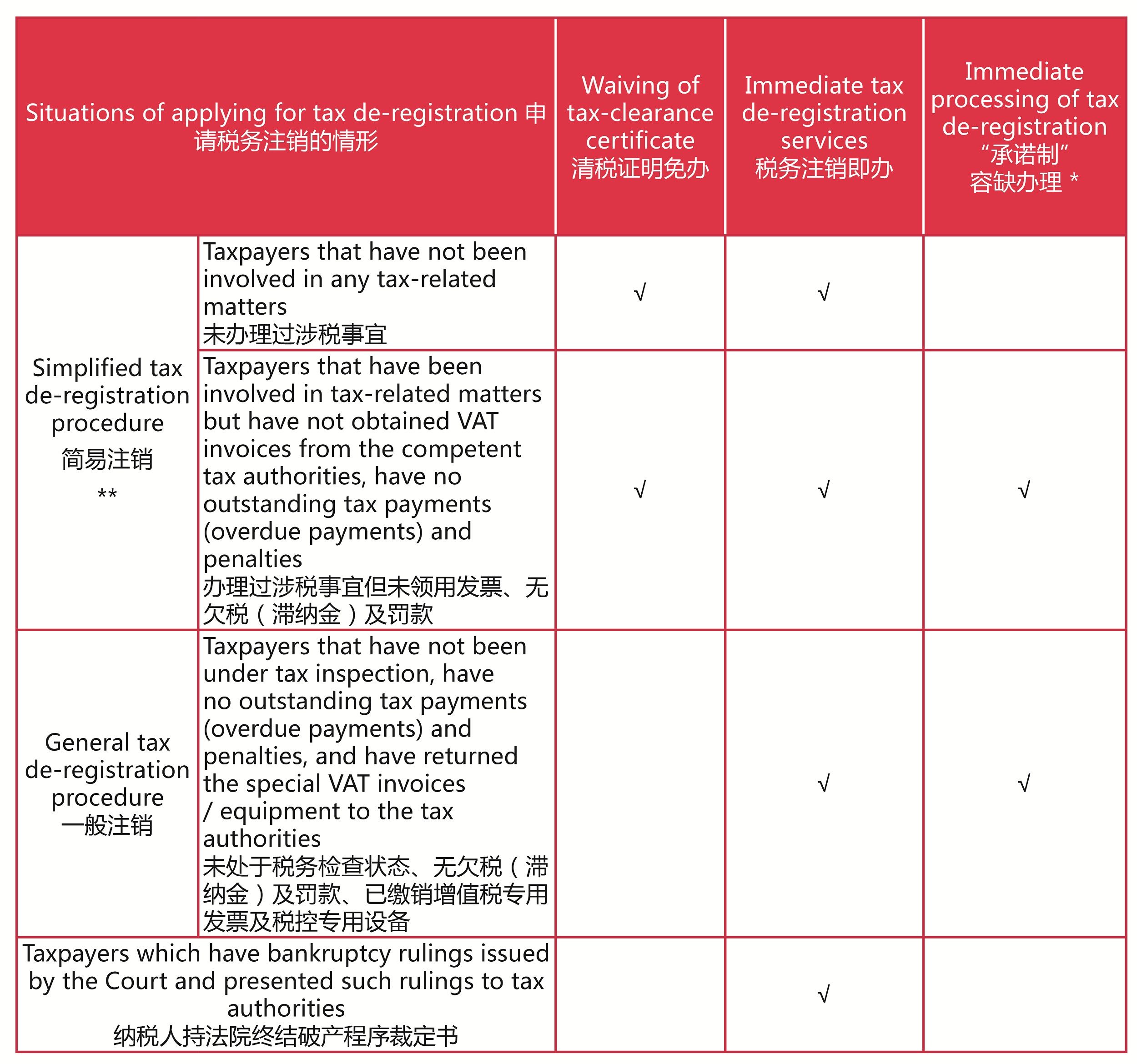

The measures to refine the tax de-registration procedures provided in Circular No. 149 and Circular No. 64 include waiving of tax-clearance certificate, optimizing the immediate tax de-registration services and simplifying tax de-registration procedures and documentation, etc. The key points are summarised in the table below:

149号文和64号文推行的优化税务注销办理程序的措施包括实行清税证明免办服务、优化税务注销即办服务、简化注销办理流程和资料等。重点内容以表格形式总结如下:

* Taxpayers that are eligible for the immediate processing of tax de-registration under the “commitment system” include: taxpayers classified as tax credit rating A or B, taxpayers classified as tax credit rating M, whose controlling parent companies are classified as tax credit rating A, enterprises incorporated by leading talents recognised by the provincial-level governments or recognised by industry associations at or above the provincial-level, self-employed industrial and commercial households that are taxed at a fixed term and amount and not included in the tax credit rating system, and taxpayers not reaching the VAT threshold.

* Taxpayers that are eligible for the immediate processing of tax de-registration under the “commitment system” include: taxpayers classified as tax credit rating A or B, taxpayers classified as tax credit rating M, whose controlling parent companies are classified as tax credit rating A, enterprises incorporated by leading talents recognised by the provincial-level governments or recognised by industry associations at or above the provincial-level, self-employed industrial and commercial households that are taxed at a fixed term and amount and not included in the tax credit rating system, and taxpayers not reaching the VAT threshold.

* 符合“承诺制”容缺办理条件的纳税人包括:纳税信用级别为A级和B级的纳税人、控股母公司纳税信用级别为A级的M级纳税人、省级政府引进人才或省以上行业协会认定的行业领军人才等创办的企业、未纳入纳税信用级别评价的定期定额个体工商户、未达到增值税纳税起征点的纳税人等五大类。

** According to the (Gongshangqizhuzi [2016] No. 253), limited liability companies, non-corporate enterprise legal persons, sole proprietorship enterprises and partnership enterprises which have not started businesses or have no credits or debts, can elect to apply to the streamlined de-registration procedure.

** 根据《关于全面推进企业简易注销登记改革的指导意见》(工商企注字[2016]253号),未开业、申请注销登记前未发生债权债务的有限责任公司、非公司企业法人、个人独资企业、合伙企业可以选择简易注销程序。

The highlight of Circular No. 64 is that tax authorities can immediately issue tax clearance certificates when taxpayers, who have declared bankrupt, apply for tax de-registration with the rulings issued by the People's Court and write off the outstanding tax underpayments of taxpayers in accordance with the relevant laws and regulations. Tax de-registration of bankrupt enterprises has always been a big practical issue in business de-registration. According to the prevailing Bankruptcy Law of China, the administrator shall, within 10 days upon the conclusion of the bankruptcy proceedings, handle the de-registration formalities at the original business registration authorities, i.e. the administrative authorities for industry and commerce (the current market supervision departments), with the ruling of the People's Court. However, according to the Tax Collection and Administration Law and its detailed implementation rules, before applying for de-registration at the administrative authorities for industry and commerce, taxpayers have to go to the in-charge tax authorities to handle tax de-registration formalities with the relevant certificates.

The highlight of Circular No. 64 is that tax authorities can immediately issue tax clearance certificates when taxpayers, who have declared bankrupt, apply for tax de-registration with the rulings issued by the People's Court and write off the outstanding tax underpayments of taxpayers in accordance with the relevant laws and regulations. Tax de-registration of bankrupt enterprises has always been a big practical issue in business de-registration. According to the prevailing Bankruptcy Law of China, the administrator shall, within 10 days upon the conclusion of the bankruptcy proceedings, handle the de-registration formalities at the original business registration authorities, i.e. the administrative authorities for industry and commerce (the current market supervision departments), with the ruling of the People's Court. However, according to the Tax Collection and Administration Law and its detailed implementation rules, before applying for de-registration at the administrative authorities for industry and commerce, taxpayers have to go to the in-charge tax authorities to handle tax de-registration formalities with the relevant certificates.

After the termination of bankruptcy, and before the tax de-registration, taxpayers have to settle the outstanding tax payments, surcharges and penalties. As most of the bankrupt enterprises are insolvent, it is almost impossible for these taxpayers to settle the outstanding tax payments, surcharges and penalties, which greatly affects the efficiency of tax de-registration of bankrupt enterprises. Circular No. 64 clearly stipulates that taxpayers, who have been declared bankrupt by the People’s Court, can present the bankruptcy rulings issued by the Court to the tax authorities in applying for tax de-registration and the tax authorities can immediately issue tax clearance certificates and write off the outstanding tax underpayments in accordance with the laws and regulations. It is a breakthrough in tax de-registration procedures for bankrupt enterprises and also an important demonstration of how the China tax authorities are advancing and implementing the law-based tax administration.

64号文最大的亮点是,依法破产的纳税人持人民法院出具的终结破产程序裁定书向税务机关申请办理税务注销,税务机关即时出具清税文书。对于纳税人仍存在的欠税,税务机关按照规定进行“死欠”核销处理。破产企业税务注销一直以来都是注销实务中的一大难题。根据现行破产法,管理人应当自破产程序终结之日起十日内,持人民法院终结破产程序的裁定,向破产人的原登记机关,即工商行政管理机关(现市场监管部门)办理注销登记。然而,根据税收征管法及实施细则有关规定,纳税人在向工商行政管理机关申请办理注销登记之前,应当持有关证件向税务机关申报办理注销税务登记;纳税人破产终结后、办理注销税务登记前,应当结清应纳税款、滞纳金和罚款。由于绝大多数破产企业属于资不抵债的情况,几乎不可能结清应纳税款、滞纳金和罚款,极大地影响破产企业办理注销的效率。64号文明确规定经法院裁定宣告破产的纳税人,持法院终结破产程序裁定书申请税务注销,税务机关即时出具清税文书并按照规定核销“死欠”,是对破产企业税务注销实务的重大突破,也是中国税务机关推进和落实依法治税的重要体现。

Circular No. 149 and Circular No. 64 also simplify the procedures and documentation requirements for tax de-registration, such as special service windows for tax de-registration, providing nil tax filing services in batches, automatic termination of "entrustment agreement between tax authorities and commercial banks", and simplifying the relevant certificates and documentation requirements for those taxpayers who have completed the identification verifications to handle tax-related matters to further reduce the compliance burdens on taxpayers.

149号文和64号文还简化税务注销办理流程和资料,例如设置注销业务专门服务窗口、提供批量零申报服务、自动终止“委托扣款协议书”,以及对实名办税的纳税人简化相关证件资料的要求等,进一步减轻纳税人的报送负担。

The takeaway

The takeaway

We are pleased to see some of the long-standing hot issues in relation to tax de-registration have received the attention of the tax authorities, and the tax de-registration procedure continues to be refined. The immediate processing of tax de-registration under the “commitment system” in Circular No. 149 is an institutional innovation based on the presumption of taxpayers’ good faith, indicating a breakthrough to reflect the philosophy of "Streamlined Administration, Delegated Powers, Improved Regulations and Services". As there was no pre-condition under the previous administrative practice of immediate processing of the tax de-registration, while allowing the taxpayers to provide the outstanding documents within an agreed time frame, in practice, some enterprises, which were allowed to be de-registered, simply did not submit the outstanding documents after the tax de-registration, which may create enforcement risks to the tax authorities. As Circular No. 149 requires a binding “commitment” from taxpayers, for taxpayers who fail to fulfil the commitments, their legal representatives and financial responsible persons shall be classified with a D tax credit rating. It cannot only ensure the smooth implementation of the immediate processing of tax de-registration, but also put forward higher compliance requirements on taxpayers.

我们很高兴地看到有关税务注销的一些长久以来的热点问题得到税务部门的关注,税务注销流程也在持续优化。作为149号文的创新举措,“承诺制”容缺办理是基于对纳税人诚信推定做出的一项制度创新,充分体现了“放管服”理念,具有很大的突破性。以前采取的容缺办理制度,因为没有前置条件,在实践中往往企业容缺办理后,不再提交补充资料,可能给税务机关造成一定的执法风险。149号文对纳税人提出“承诺”约束,对未履行承诺的纳税人,税务机关将对其法定代表人、财务负责人纳入纳税信用D级管理,不仅为容缺办理的顺利实施提供制度保障,对纳税人税务遵从也提出更高的要求。

Due to different understandings of the policies in Circular No. 149 and Circular No. 64, local practices of the tax de-registration procedures may vary among different tax authorities. Considering Circular No. 64 will take effect from 1st of July, 2019, we suggest that taxpayers should actively communicate with the in-charge tax authorities and confirm the procedure and documentation requirements of tax de-registration in advance, so as to avoid "multiple trips" in the tax authorities.

Due to different understandings of the policies in Circular No. 149 and Circular No. 64, local practices of the tax de-registration procedures may vary among different tax authorities. Considering Circular No. 64 will take effect from 1st of July, 2019, we suggest that taxpayers should actively communicate with the in-charge tax authorities and confirm the procedure and documentation requirements of tax de-registration in advance, so as to avoid "multiple trips" in the tax authorities.

由于对149号文和64号文政策的理解不同,各地税务机关在为纳税人办理税务注销手续时在执行口径上可能存在差别。考虑到64号文将于2019年7月1日起实行,我们建议企业在办理税务注销之前,应积极与主管税务机关沟通,事先确认好办理税务注销的流程和资料要求,以避免“多次跑”的情况。

It should be noted that, except for the situation of bankruptcy declaration by the People's Court in Circular No. 64, one of the preconditions of general tax de-registration procedure for enterprises is no outstanding tax underpayment. Before applying for tax de-registration, enterprises should not neglect the compliance risks and should review the various types of taxes to ensure that they have been properly settled in accordance with the relevant laws and regulations.

应注意的是,除64号文所述经人民法院裁定宣告破产的情形外,一般企业税务注销的前提之一是无欠税。这些企业在办理税务注销前仍需要检视各类税种是否需要按照相关的法规进行税务清算,是否有需要补缴的欠税,不应忽视相关的合规风险。