Mainland and the HKSAR signed the Fifth Protocol to the Mainland

HK Double Taxation Arrangement

By Kelvin Lee, PwC

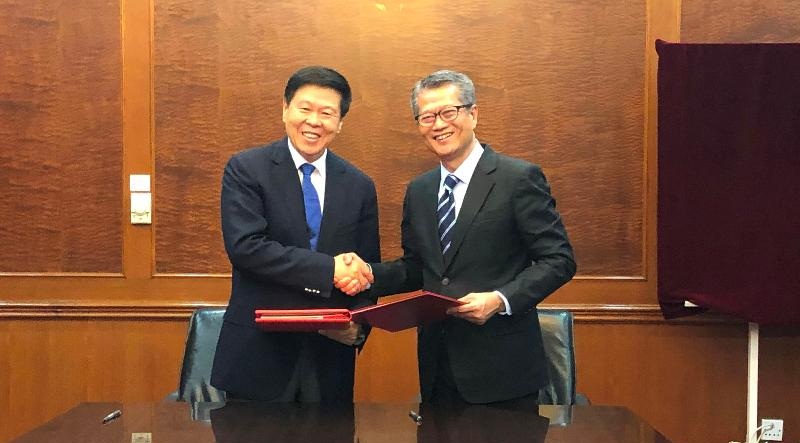

On 19th of July, 2019, the Commissioner of the State Taxation Administration (“STA”), Mr. Wang Jun, and the Financial Secretary of the Hong Kong Special Administrative Region (“Hong Kong”, or “HKSAR”), Mr. Paul Chan, signed the Fifth Protocol to the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income (“Mainland/HK DTA”) (“the Fifth Protocol”) in Beijing. The Fifth Protocol will enter into force upon the written notifications by both sides of the completion of their respective required ratification processes.

On 19th of July, 2019, the Commissioner of the State Taxation Administration (“STA”), Mr. Wang Jun, and the Financial Secretary of the Hong Kong Special Administrative Region (“Hong Kong”, or “HKSAR”), Mr. Paul Chan, signed the Fifth Protocol to the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income (“Mainland/HK DTA”) (“the Fifth Protocol”) in Beijing. The Fifth Protocol will enter into force upon the written notifications by both sides of the completion of their respective required ratification processes.

2019年7月19日,国家税务总局(“国税总局”)局长王军与香港特别行政区财政司司长陈茂波在北京签署了《内地和香港特别行政区关于对所得避免双重征税和防止偷漏税的安排》(“内地与香港税收安排”)第五议定书(“第五议定书”)。第五议定书将在双方各自履行必要的批准程序并互相书面通知后生效。

The Fifth Protocol mainly introduces changes in the following two areas:

The Fifth Protocol mainly introduces changes in the following two areas:

第五议定书主要有以下两部分内容:

• Incorporating the recommendations in the Base Erosion and Profit Shifting (“BEPS”) action reports released by the Organisation for Economic Co-operation and Development (“OECD”), including amending the preamble and articles, such as Resident, Permanent establishment, Capital gains, etc., and adding a new ‘principal purposes test’ (“PPT”) article on prevention of treaty abuse;

纳入了经济合作与发展组织(“OECD”)税基侵蚀与利润转移(“BEPS”)行动计划的相关成果,修改了序言、居民、常设机构、财产收益等条款,新增了“享受安排优惠的资格判定”条款。

• Adding a new “Teachers and researchers” article to grant tax exemption to teachers or researchers of one side for eligible remuneration received for services performed on the other side.

新增“教师和研究人员”条款,给予一方的教师和研究人员在另一方工作取得的符合条件的所得免税待遇。

In this article, we have summarized the main contents of the Fifth Protocol, analysed the impact from both Mainland and Hong Kong tax perspective, as well as shared with you our observations.

在本文中,我们总结了第五议定书的主要内容,并分别从香港税收居民在内地的税收影响、内地税收居民在香港的税收影响两个角度分享我们的观察。

The main contents of the Fifth Protocol and its impact from the Mainland and Hong Kong tax perspective

第五议定书的主要内容及对内地、香港的税收影响

Article 4 Resident

Article 4 Resident

The existing Mainland/HK DTA provides a tie-breaker rule for determining the residency status of a person other than an individual who is a tax resident of both sides, which looks at the person’s place of effective management. The Fifth Protocol amends the above tie-breaker rule and replaces it with the provision that the STA and Hong Kong Inland Revenue Department (“Hong Kong IRD”) shall endeavour to determine the tax residency of such person by mutual agreement by taking into accounts its place of effective management, the place where it is incorporated, or otherwise constituted (and any other relevant factors). In the absence of such agreement, such person shall not be entitled to any relief or exemption from tax provided by the Mainland/HK DTA.

第四条 居民

第五议定书修改了对于除个人以外的双重居民实体的加比规则。按照现行的内地与香港税收安排的规定,若某企业同时构成内地和香港双方的税收居民,应按其实际管理机构所在地认定为一方的居民企业。

按照第五议定书,国税总局和香港税务局应通过其实际管理机构所在地、其注册地、或成立地(以及其他相关因素的基础上),尽力通过协商确定该企业应被视为内地居民还是香港居民以适用税收安排优惠。如双方税局未能就该企业居民身份达成一致意见,该企业不能享受安排规定的任何税收优惠或减免。

Article 5 Permanent Establishment

Article 5 Permanent Establishment

The Fifth Protocol adopts the recommendations in the final report of BEPS Action 7 (preventing the artificial avoidance of permanent establishment status), which introduces a stricter definition for Permanent Establishment (“PE”) constituted through an agent (“Agency PE”):

• Widening the scope of Agency PE: Under the existing Mainland/HK DTA, where a person is acting in the Mainland on behalf of a Hong Kong enterprise, and habitually exercising an authority to conclude contracts in the name of the Hong Kong enterprise, the Hong Kong enterprise shall be deemed to have a PE in the Mainland. The Fifth Protocol expands the scope of Agency PE to include not only “conclusion” of contracts, but also habitually “plays the principal role leading to the conclusion of contracts” (that are routinely concluded without material modification by the Hong Kong enterprise), and the Hong Kong enterprise shall be deemed to have a PE in the Mainland if these contracts are:

1. In the name of the Hong Kong enterprise; or

2. Not in the name of the Hong Kong enterprise, but for the transfer of the ownership of, or for the granting of the right to use, property owned by that Hong Kong enterprise or that Hong Kong enterprise has the right to use; or

3. Not in the name of the Hong Kong enterprise, but for the provision of services by that Hong Kong enterprise.

Under the existing Mainland/HK DTA, Agency PE only covers the above-mentioned type 1) situation. When the Fifth Protocol comes into effect, even if the contract is not concluded in the name of the Hong Kong enterprise, the Hong Kong enterprise may still be deemed to have a PE in the Mainland through the commissionaire arrangement as described in above-mentioned type 2) and 3) situations. Although the OECD has quite lengthy discussion on commissionaire arrangement, neither the STA nor HKIRD has officially released their interpretations on such arrangement. In that respect, there are uncertainties on how both tax authorities would deal with above-mentioned type 2) and 3) Agency PE.

• Stricter definition for “independent agent”: A Hong Kong enterprise would not create an “Agency PE” in the Mainland if it engages an independent agent to carry out the above mentioned activities in the Mainland. The Fifth Protocol provides a much stricter definition for independent agent, which states that if a person “acts exclusively or almost exclusively on behalf of one or more enterprises to which it is closely related”, that person shall not be considered to be an independent agent. It further states that “closely related” refers to direct or indirect control of more than 50%.

Indeed, in Guoshuifa [2010] No.75, the STA has already adopted a relatively strict interpretation of an Agency PE. The wording in the Fifth Protocol largely follows the recommendations in BEPS Action 7 report.

From the perspective of the Hong Kong PE risks of Mainland tax residents: the widened scope of Agency PE is also applicable to a person acting in Hong Kong on behalf of a Mainland enterprise. If a person negotiates contracts in Hong Kong on behalf of a Mainland enterprise, even if such person does not “conclude” the contracts, there is still risk for the Mainland enterprise being deemed as having a PE in Hong Kong. It is the first time for the HKSAR to adopt such recommendations in the BEPS Action 7 report in a Hong Kong DTA.

第五条 常设机构

第五条 常设机构

第五议定书采纳了BEPS第7项行动计划《防止人为规避构成常设机构》的建议,使代理型常设机构的定义更为严格:

• 扩大了代理型常设机构的定义:按照现行的内地与香港税收安排的规定,一个人在内地代表香港企业进行活动,如果该人有权以香港企业的名义签订合同并经常行使这种权力,则该香港企业会被视为在内地构成常设机构。

第五议定书将代理型常设机构的定义扩大到不仅仅是“订立合同”,如果该人经常性地在合同订立过程中“发挥主要作用”(而香港企业不对合同做实质性修改),且相关合同属于以下情形之一的,该香港企业会被视为在内地构成常设机构:

(一)合同以该香港企业的名义订立,或

(二)合同虽不由香港企业的名义订立,但涉及该香港企业拥有或有权使用的财产的所有权转让或使用权授予;或

(三)合同虽不由香港企业的名义订立,但涉及由该香港企业提供服务。

在现行的内地与香港税收安排下,代理型常设机构通常只涵盖情形(一)的情况。经过此次修订,即使合同不以香港企业的名义签订,仍有在内地构成常设机构的可能。然而对情形(二)和情形(三)所述的佣金代理人的安排,虽然OECD层面有过较多讨论,但是双方税务局均未发布过相关解释,在执行中如何理解可能还存在较多不确定因素。

• 独立代理人的定义更为严格:香港企业聘请的独立代理人在内地从事的活动不会构成香港企业在内地的常设机构。第五议定书收紧了独立代理人的定义,规定“专门或者几乎专门代表一个或多个与其紧密关联的企业进行活动”的人不属于独立代理人。同时还定义了“紧密关联的企业”是指直接或间接控制权超过50%。

事实上,国税总局早在国税发[2010]75号文中就已经针对代理型常设机构的判定口径做了较为严格的解释,第五议定书则参考了BEPS第7项行动计划建议的行文方式。

从内地居民企业在香港的常设机构风险来看:以上扩大了的代理型常设机构定义同样适用于一个人在香港代表内地企业进行活动。这意味着日后该人若在香港从事合同洽谈活动,即使没有订立合同,亦有可能被视为在香港构成常设机构。第五议定书使得内地与香港税收安排成为香港特别行政区政府签署的首份采纳了BEPS第7项行动计划建议的税收协定/安排。

Article 13 Capital Gains

Article 13 Capital Gains

The Fifth Protocol applies a more precise wording for gains from the alienation of shares. According to the existing Mainland/HK DTA, gains derived by a Hong Kong tax resident from the alienation of shares in a company may be taxed in the Mainland, if at any time within the 3 years before the alienation, these shares derived not less than 50% of the value, directly or indirectly, from immovable property situated in the Mainland. The Fifth Protocol clarifies that this article applies not only to shares in a company, but also to comparable interests, such as interests in a partnership or trust. In other words, the Mainland is granted the right to tax the relevant gains from alienation of such comparable interests derived by a Hong Kong resident.

In addition, the Fifth Protocol slightly changes the percentage of value derived from immovable property from “not less than 50%” to “more than 50%”.

According to the international practice, “the (shares of a) company, (interests in a) partnership or trust” refers to a company, a partnership, a trust established anywhere in the world.

Although the Mainland/HK DTA grants the relevant taxing rights to the Mainland, it is also necessary to consider the relevant provisions under the Mainland's Corporate Income Tax (“CIT”) law and the Individual Income Tax (“IIT”) Law to determine whether the relevant gains should be subject to tax under the “domestic law” in the Mainland.

From the Hong Kong tax perspective of a Mainland tax resident: Similarly, even the Fifth Protocol grants the taxing right to Hong Kong on such relevant gains (for example, gains derived by a Mainland investor from transfer of interests in a trust mainly invested in Hong Kong real estate), the relevant provisions of Hong Kong Inland Revenue Ordinance (“IRO”) would still need to be considered in determining whether such gains are subject to tax in Hong Kong.

In addition, the Fifth Protocol also clarifies that the term “immovable property” in this clause should be by reference to the definition of “Immovable Property” in Article 6 of the Mainland/HK DTA, which is consistent with international practice.

第十三条 财产收益

对于转让以不动产为主的股份收益的征税权的描述,第五议定书的行文更加严格。根据现行内地与香港税收安排,当被转让企业的股权价值在转让前三年内,至少50%直接或间接由位于内地的不动产构成时,内地有征税权。第五议定书明确此条款不仅仅适用于企业股权的转让,合伙或信托权益的转让同样可以适用本条款,即内地对相关收益也有征税权。第五议定书亦将不动产的百分比由“至少50%”稍微调整为“超过50%”。按照国际惯例,该条款所称的“股份、合伙、信托”是泛指在任何地方设立的公司、合伙和信托。

虽然内地与香港税收安排赋予内地相关的征税权,还需结合内地的企业所得税法和个人所得税法的相关规定,具体判断相关转让收益是否按照内地“本土法”应在内地缴纳所得税。

从内地税收居民在香港的税收角度来看:同样地,从香港税务角度而言,即使第五议定书将相关收益(例如内地居民转让主要投资在香港房地产的信托权益取得的收益)的征税权赋予香港,该收益是否须要在香港征税仍须考虑香港“本土法”的相关规定。

此外,第五议定书还明确本条款的“不动产”应参照内地与香港税收安排的第六条“不动产”条款的定义去理解,这也符合一贯的国际惯例。

Article 18 (A) Teachers & Researchers

Article 18 (A) Teachers & Researchers

The existing Mainland/Hong Kong DTA does not have an article dealing with teachers or researchers. The Fifth Protocol introduces Article 18(A), which provides individual income tax exemption for a period of 3 years for remuneration received by a Hong Kong resident individual employed by a university, institute, school in Hong Kong, or any other educational or research institution officially recognized in Hong Kong (“eligible institution”) from his Hong Kong employer and who stays in the Mainland mainly for the purpose of teaching or engaging in research in an eligible institution in the Mainland, provided that such remuneration is taxable in Hong Kong. After the expiration of the exemption period, such remuneration would be taxable in the Mainland according to the STA’s interpretation.

In response to this new article, the HKIRD has also amended the Hong Kong IRO recently to introduce Section 8(1AB). The effect of the section is that for a Hong Kong resident individual who derives income from services rendered by him/her as a teacher or researcher in the Mainland, if he/she has enjoyed tax exemption on the above mentioned income under the Mainland/HK DTA, then even if his/her “visits” to Hong Kong are not more than 60 days in the year of assessment concerned, he/she will not be eligible for the “60-Day Rule” exemption1 under the Hong Kong IRO. The amendment is to prevent “double non-taxation”.

STA Public Notice [2016] No.91 has provided the scope of eligible institutions. Specifically, except for training institutions, schools offering pre-school education, elementary education, secondary education, higher education and special education are all eligible.

From the Hong Kong tax perspective of a Mainland tax resident: Similarly, if a Mainland teacher or researcher receives remuneration from his/her Mainland employer for teaching or engaging in research in an eligible institution in Hong Kong and pays IIT on the remuneration, such remuneration is exempt from salary tax in Hong Kong for a period of 3 years.

The introduction of Article 18(A) is good news to teachers and researchers engaging in teaching and research activities on both sides. It will promote academic exchange and scientific research collaboration between the Mainland and Hong Kong, especially it will increase the competitiveness of Mainland educational institutions in attracting education and research talents from Hong Kong.

第十八条(附)教师和研究人员

现行内地与香港税收安排并没有关于教师和研究人员的条款。第五议定书新增这一条款,规定受雇于香港的大学、学院、学校或政府认可的教育机构或科研机构(“合资格院校”)的香港税收居民个人到内地合资格院校从事教学或研究取得的由香港雇主支付的报酬,如果该报酬在香港征税,则可以在三年内在内地享受免税的待遇。按照国税总局的执行口径,超过免税期的,从超过之日起内地可以征税。

针对这项新增条款,香港也已于较早前修订《香港税务条例》,加入第8(1AB)条,明确对于上述情况,即一名香港税收居民个人受雇于香港雇主但主要工作地点在内地,并就上述报酬于内地享受了免税待遇,即使该人在有关课税年度“到访”香港不超过60日,该个人的该报酬也不可以享受香港税法下“不超过60日”的税务豁免1,以防止“双重免税”。

国家税务总局公告[2016]91号已就合资格院校的定义和范围作了规范,具体来说在内地除了培训机构不属于合资格院校以外,学前教育、初等教育、中等教育、高等教育和特殊教育的学校都可适用该条款。

从内地税收居民个人在香港的税收角度来看:同样地,作为内地税收居民的教师和研究人员到香港合资格院校从事有关教学或研究工作,获得内地雇主支付的报酬并就该工作报酬在内地交税,则可以在三年内在香港享受免税的待遇。

新增的“教师和研究人员”条款对于两地从事教学、研究的老师和研究人员来说无疑是一项利好消息,有助两地学术和研发交流,尤其是加强内地教育机构在吸引香港教育科研人才方面的竞争力。

Article 24 (A) Entitlement to Benefits

Article 24 (A) Entitlement to Benefits

To prevent the abusive use of tax treaty, the Fifth Protocol amends the language used in the preamble of the Mainland/HK DTA, which emphasizes that in addition to the elimination of double taxation, the purpose of the Mainland/HK DTA is also to prevent non-taxation or reduced taxation through tax evasion or avoidance.

The Fifth Protocol also adds a new Article 24(A), the principal purposes test (PPT) article, under which a benefit under the Mainland/HK DTA shall not be granted in respect of an item of income if it is reasonable to conclude, having regard to all relevant facts and circumstances, that obtaining that benefit was one of the principal purposes of any arrangement or transaction that resulted directly or indirectly in that benefit, unless it is established that granting that benefit in these circumstances would be in accordance with the object and purpose of the relevant provisions of this DTA.

序言以及第二十四条(附)享受安排优惠的资格判定

为防止协定滥用,第五议定书对内地与香港税收安排的序言进行了修改,增加了关于防止避税的表述,强调了税收安排的目的除了消除双重征税,也为了防止通过逃避税行为造成不征税或少征税。

同时第五议定书新增“享受安排优惠的资格判定”条款,即“主要目的测试”条款:“如果在考虑了所有相关事实与情况后,可以合理地认定任何直接或间接带来本安排优惠的安排或交易的主要目的之一是获得该优惠,则不得就相关所得给予该优惠,除非能够确认在此等情况下给予该优惠符合本安排相关规定的宗旨和目的”。

The takeaway

The takeaway

On 7th of June, 2017, the STA attended the OECD signing ceremony on the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (“MLI”) and signed the MLI on behalf of both China and the HKSAR. Thereafter, China and the HKSAR have respectively released their provisional MLI positions. The aim of the MLI is to swiftly modify bilateral tax treaties to implement treaty-related BEPS recommendations. As the Mainland/HK DTA is not a tax agreement between two sovereign countries, it is not covered by the MLI.

The Mainland and Hong Kong have gone through bilateral negotiation of the Fifth Protocol, which amends the relevant articles in the Mainland/HK DTA to incorporate the relevant suggestions in the MLI that both sides have agreed to, resulting in more stringent requirements on anti-tax avoidance3. Enterprises and individuals conducting cross-border business in the Mainland and Hong Kong should comply with new changes in international tax practice to mitigate cross-border tax risks and enhance tax compliance.

The relevant tax benefits provided by the newly added "Teachers and Researchers" article should facilitate the flow of teachers and researchers between the Mainland and Hong Kong. It is particularly beneficial for cooperative education projects in the Guangdong-Hong Kong-Macao Greater Bay Area (“GBA”). It will support the educational institutions to jointly build superior faculties, laboratories and research centres in the GBA, promote scientific and technological development, improve educational cooperation and exchange of talents mechanism, and promote the development of the GBA. However, Hong Kong's educational institutions participating in cooperative education projects in the Mainland will still need to be mindful of their CIT exposures due to the potential PE risks in the Mainland.

中国政府于2017年6月7日出席了由OECD举行的《实施税收协定相关措施以防止税基侵蚀和利润转移的多边公约》(“多边工具”)的联合签字仪式,代表中国及香港特别行政区签订了“多边工具”。双方随后发布了各自的立场文书。多边工具旨在迅速修订双边税收协定以实施相关的BEPS行动建议。由于内地与香港税收安排并不是两个主权国家间所签署的,因此没有被纳入多边工具所涵盖的税收协定中。

内地与香港通过双边协商,在第五议定书中就多边工具的部分内容达成的共识修订了税收安排中的相关条款4,对反避税要求更趋严格。在两地开展跨境业务的企业和个人应顺应国际税收规则的新变化,以更好地应对跨境税收风险,增强税收合规性。

新增的“教师和研究人员”条款的相关优惠可以有效支持内地和香港两地间教师和研究人员的流动,尤其有利于粤港澳高校合作办学,联合共建优势学科、实验室和研究中心,推动两地科学技术进步,完善教育合作交流机制,助力粤港澳大湾区发展。然而,香港的教育机构在内地开展合作办学,仍需要关注可能在内地构成常设机构引起的企业所得税风险。