Striking back against the outbreak of COVID-19

A series of fiscal and taxation policies to prevent and control the epidemic were released

【防疫应变】

财税部门重磅发力,聚焦疫情防控

By Kelvin Lee, PwC

In response to the severe epidemic situation of the novel coronavirus pneumonia (COVID-19), Chinese governments at all levels rapidly issued several policies to control the epidemic and support the economy. On February 5, the executive meeting of the State Council decided to launch a series of fiscal and taxation policies in addition to the previously introduced measures, to ensure that there are sufficient supplies for the epidemic prevention and control work, effective from 1 January 2020.

In response to the severe epidemic situation of the novel coronavirus pneumonia (COVID-19), Chinese governments at all levels rapidly issued several policies to control the epidemic and support the economy. On February 5, the executive meeting of the State Council decided to launch a series of fiscal and taxation policies in addition to the previously introduced measures, to ensure that there are sufficient supplies for the epidemic prevention and control work, effective from 1 January 2020.

为了应对严峻的新型冠状病毒感染的肺炎疫情,中国各级政府部门迅速响应,出台了多项政策文件以控制疫情、支持经济。2月5日召开的国务院常务会议决定,在前期针对疫情防控已出台各方面措施的基础上,再推出一批支持保供的财税金融政策,自2020年1月1日起实施。

On February 7, the Ministry of Finance (MOF) issued four policies jointly with other departments:

On February 7, the Ministry of Finance (MOF) issued four policies jointly with other departments:

2月7日,财政部会同多部门,共同发布了四项政策:

• Public Notice Jointly Issued by the MOF and State Taxation Administration (STA) Regarding Tax Policies to Prevent and Control the Outbreak of COVID-19 (the MOF and STA Public Notice [2020] No. 8)

• 财政部、税务总局关于支持新型冠状病毒感染的肺炎疫情防控有关税收政策的公告(财政部、税务总局公告[2020]8号)

• Public Notice Jointly Issued by the MOF and STA Regarding Tax Policies for Donations to Prevent and Control the Outbreak of COVID-19 (the MOF and STA Public Notice [2020] No. 9)

• 财政部、税务总局关于支持新型冠状病毒感染的肺炎疫情防控有关捐赠税收政策的公告(财政部、税务总局公告[2020]9号)

• Public Notice Jointly Issued by the MOF and STA Regarding Individual Income Tax Policies to Prevent and Control the Outbreak of COVID-19 (the MOF and STA Public Notice [2020] No. 10)

• 财政部、税务总局关于支持新型冠状病毒感染的肺炎疫情防控有关个人所得税政策的公告(财政部、税务总局公告[2020]10号)

• Public Notice Jointly Issued by the MOF and the National Development and Reform Commission (NDRC) Regarding the Exemption of Certain Administrative Fees and Government-managed Funds (the MOF and NDRC Public Notice [2020] No. 11)

• 财政部、国家发展改革委关于新型冠状病毒感染的肺炎疫情防控期间免征部分行政事业性收费和政府性基金的公告(财政部、国家发展改革委公告[2020]11号)

The policies focus on manufacturers of epidemic prevention and control supplies, relevant transportation companies and medical companies, etc., and aim at lowering the production and operation cost for the relevant enterprises, energising the expansion of supply of epidemic prevention materials, and medical and pharmaceutical supplies. We will share with you the key points of these tax policies and our insights.

The policies focus on manufacturers of epidemic prevention and control supplies, relevant transportation companies and medical companies, etc., and aim at lowering the production and operation cost for the relevant enterprises, energising the expansion of supply of epidemic prevention materials, and medical and pharmaceutical supplies. We will share with you the key points of these tax policies and our insights.

政策主要着力于防疫用品生产企业、相关运输物流企业、医疗企业等,助力相关企业进一步降低生产运营成本,推动防疫物资和医药产品加大供给,为坚决打赢疫情防控阻击战提供更好支撑。在本期中,普华永道将与您分享相关税收政策要点及我们的观察,助力大家共渡难关!

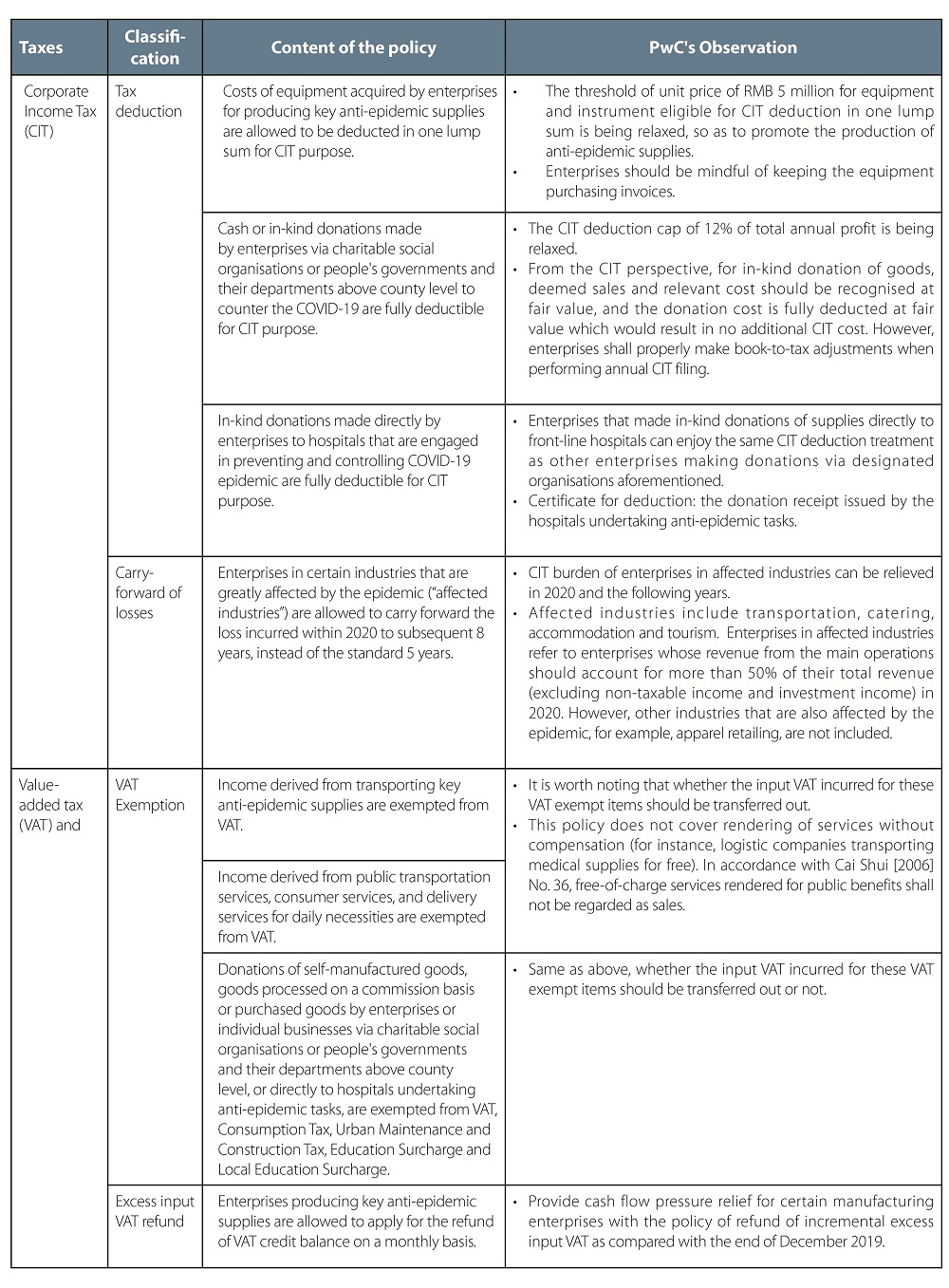

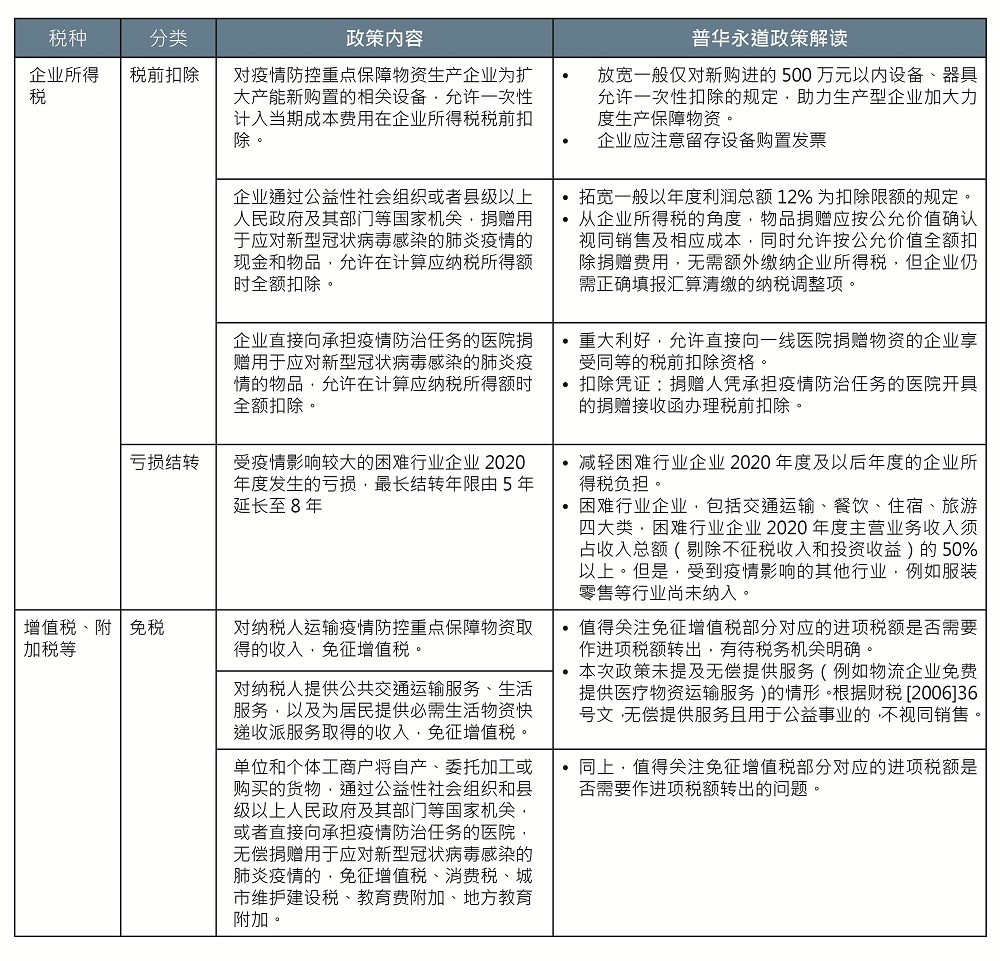

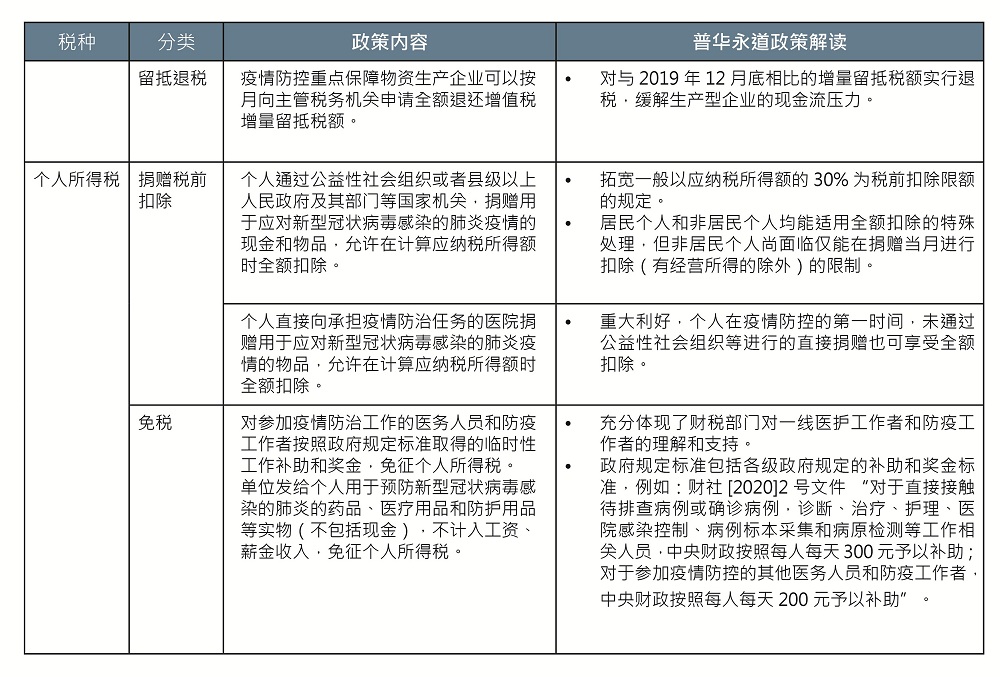

In the table below, we summarised the relevant tax policies (MOF and STA Public Notice [2020] No. 8, 9 and 10) and insights for your reference.

我们在下表中整合了相关税政(8、9、10号公告)要点及我们的观察,供您参考。

The takeaway

The takeaway

注意要点

In the process of implementing the above policies, we expect relevant authorities to define the list of "enterprises producing key anti-epidemic supplies" and the specific scope of "key anti-epidemic supplies" as soon as possible. In accordance with the Urgent Circular on Strengthening the Funding Support for Enterprises Producing Key Anti-Epidemic Supplies (Cai Jin [2020] No. 5) issued in the evening of 7 February jointly by the MOF, NDRC, Ministry of Industry and Information Technology, People's Bank of China, and the National Audit Office, provincial authorities can issue the list of local qualified enterprises on their own. It is recommended that the process for enterprises' independent application should be implemented as soon as possible, as well as allow special process in case of emergency. In addition, we also suggest that relevant local government departments and tax authorities should actively publicise and promote the aforementioned policies and implementation measures to taxpayers through online channels.

在落地执行上述政策的过程中,我们期待相关部门尽快落实“疫情防控重点保障物资生产企业”的名单和“疫情防控重点保障物资”的具体范围。根据2月7日晚发布的《财政部、发展改革委、工业和信息化部、人民银行、审计署关于打赢疫情防控阻击战强化疫情防控重点保障企业资金支持的紧急通知》(财金[2020]5号),省级相关部门可自主建立地方性企业名单,建议尽快落地企业自主申请等操作流程,紧急情况下允许特事特办。另外,我们也建议各地相关政府机构和税务机关通过线上渠道主动向纳税人宣传和推送这些政策及落地口径。

In order to ensure that enterprises can enjoy these policies, relevant enterprises need to review the completeness of their financial accounting and tax compliance. Take excess input VAT refund as an example, on the one hand, enterprises should prove their qualification of "enterprises producing key anti-epidemic supplies" with well-prepared documents; on the other hand, enterprises must pay attention to the accuracy of their accounting of input and output VAT, including the accuracy of the recognition of taxable income and the appropriateness of the historical taxable income, to accurately calculate the amount of tax refund and communicate tax refund affairs with the in-charge tax authorities as soon as possible. For the exemption policy with industry restrictions, enterprises should pay attention to whether their main operations fall within the exemption scope. Enterprises and individuals that have donated goods should pay attention to the keeping and submission of purchasing invoices, so that charitable social organisations and hospitals can determine the value of donated goods according to the invoices and issue donation receipts or donation acceptance letters.

为确保企业实实在在享受到这些政策,相关企业需审查自身财务核算的完备性和税务申报的合规性,例如对于留抵退税政策,一方面,相关企业需要准备好材料,以证明符合“疫情防控重点保障物资生产企业”资格;另一方面,企业应注意对于进项销项的核算准确性,包括应税收入确认的准确程度和历史应税收入数额的合理性,以准确计算退税金额,尽快和税务机关沟通退税事宜。对于有行业限制的免税政策,企业需注意判断自己的主营业务类型是否在政策的范围内。捐赠了物资的企业和个人,需注意保存并提交购买物资的采购发票,以便公益性社会组织和医院依据采购发票确定受赠物资价值并开具捐赠票据或捐赠接收函。

In addition, to address the epidemic outbreak and its economic impact, we also expect authorities at all levels to continue to provide a larger scale of fiscal and taxation support to industries greatly affected by the epidemic (including but not limited to transportation, catering, accommodation, tourism, apparel retailing and other industries) and other enterprises that are not able to resume operation in time or in full capacity. At present, commonly concerned issues include: exemption and relief of Real Estate Tax and Urban Land Use Tax for trouble enterprises; considering the feasibility to lower the social security contribution rate by stages in addition to the delay of payment of enterprises' social security contribution; strengthening tax support for small and micro enterprises; increasing the deduction of R&D expenses related to epidemic in medical institutions and scientific research institutions by stages; granting the same excess input VAT refund policy to other R&D enterprises related to epidemic prevention and other enterprises greatly affected by epidemic. PwC will follow up on the financial and taxation policies relating to the prevention and control of epidemic, and share with you timely.

在上述政策之外,面对此次疫情及其经济影响,我们也期望各级财税部门后续继续对受疫情影响特别重大的行业(包括且不限于交通运输、餐饮、住宿、旅游、服装零售等诸多行业)企业和其他未能及时充分复工复产的企业提供更大程度的财税支援。目前业内集中关注的方面主要包括:对房产税和城镇土地使用税实行困难减免;在缓交企业社保的基础上考虑继续阶段性降低社保费率;加大对小微企业的税收扶持力度;阶段性提升医疗机构、科研机构发生的与疫情相关的研发费用扣除比例;除“疫情防控重点保障物资生产企业”之外,对其他防疫相关的研发企业、受疫情影响重大的行业企业同样允许享受增值税增量留抵退税政策等。普华永道也将持续关注疫情防控相关的财税政策,并及时与您分享。