Recovering faster than any other major economy

We remain optimistic about the long term relations with U.S.

By Morgan Brady

Even as many in Beijing recognize that relations with the U.S. have reached a historic low, some scholars at a government-linked think tank remain optimistic about the long term.

Even as many in Beijing recognize that relations with the U.S. have reached a historic low, some scholars at a government-linked think tank remain optimistic about the long term.

“I personally have ... confidence in China-U.S. relations,” said Ruan Zongze, executive vice president at the China Institute of International Studies. “I believe that now the U.S. is actually in an abnormal state, and I believe that it’s only a short (term) phenomenon and it is an irregular state of the United States now,” Ruan said. The institute is the think tank of China’s Ministry of Foreign Affairs.

The remarks came shortly before China’s Ministry of Foreign Affairs announced that the U.S. Consulate General in the southwestern city of Chengdu must close, in retaliation to news that U.S. President Donald Trump’s administration has ordered China to close its consulate in Houston.

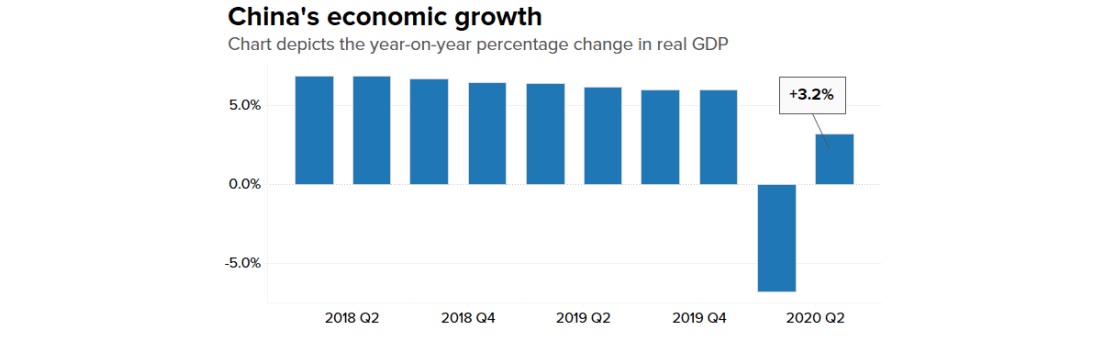

In the economic arena, China’s gross domestic product (GDP) was better than expected in the second quarter of this year, and showed to the world that its economy has rebounded quickly from the ravages of COVID-19. In the second quarter of 2020, the GDP expanded by 11.5% versus same quarter in 2019, and after a 10% contraction in the first quarter. It is a clear V-shaped recovery, which few thought possible just a few months ago.

In the economic arena, China’s gross domestic product (GDP) was better than expected in the second quarter of this year, and showed to the world that its economy has rebounded quickly from the ravages of COVID-19. In the second quarter of 2020, the GDP expanded by 11.5% versus same quarter in 2019, and after a 10% contraction in the first quarter. It is a clear V-shaped recovery, which few thought possible just a few months ago.

Furthermore, there is a multi-speed recovery across the different sectors of the economy, and supply has outpaced demand, investment has outgrown consumption, though the industrial sectors have fared better than the tertiary sectors. This difference in recovery is partly a result of the responses to the pandemic in each sector. Resuming production in many industrial and manufacturing firms was as simple as pressing the restart button. However, to revive consumption, households need to feel safe enough to return to social activity, and the lingering fear of COVID-19 relapses has slowed normalisation.

Also contributing to uneven growth has been Beijing’s policy stimulus. The design of China’s stimulus package disproportionately benefited the industrial sectors, with much policy effort devoted to work resumption, infrastructure investment and lowering funding costs, thus unintentionally benefiting the property market and housing construction.

In contrast, households do not benefit directly from the stimulus and thus, with labour market conditions and wage growth slow to recover, consumer spending has been held back.

The different designs of policy stimulus could explain, in part, the different shapes of recovery across major economies. In the United States, for example, significant policy easing has been devoted to saving jobs and subsidising income losses. This led to a strong rebound in consumer spending in May, although the latest virus resurgence could set this economic normalisation back.

The different designs of policy stimulus could explain, in part, the different shapes of recovery across major economies. In the United States, for example, significant policy easing has been devoted to saving jobs and subsidising income losses. This led to a strong rebound in consumer spending in May, although the latest virus resurgence could set this economic normalisation back.

Meanwhile, China’s priority was placed on restarting production in industrial and manufacturing firms, leaving consumption a laggard in the recovery process. This different recovery has two implications for China’s economic outlook. Firstly, an incremental rebalancing of growth drivers is likely in the second half of the year. While both infrastructure and property investment will possibly remain resilient, supported by policy easing, a gradual normalisation of job and income growth should help to unleash pent-up demand from households, allowing consumption growth to catch up.

An obvious assumption in this statement is that the virus does not appear again, and the risk is not to be underestimated as the northern hemisphere enters the colder season.

Probably, the policy easing will continue for the rest of the year, because not only do risks of renewed virus outbreaks linger, many provinces in southern China are also suffering from severe floods that have destroyed farmland, disrupted businesses, and damaged thousands of homes, affecting millions.

Assuming the floods can be brought under control in the coming weeks, the near-term economic damage should be manageable, to the tune of approximately 0.3% of GDP. However, if the severe rainfalls continue and the local authorities mishandle the emergency response, the economic shock could be exacerbated. We believe authorities will control these risks and stand ready to prevent a derailing of the economic recovery.

Assuming the floods can be brought under control in the coming weeks, the near-term economic damage should be manageable, to the tune of approximately 0.3% of GDP. However, if the severe rainfalls continue and the local authorities mishandle the emergency response, the economic shock could be exacerbated. We believe authorities will control these risks and stand ready to prevent a derailing of the economic recovery.

China’s economy is already on track to recoup its COVID-19-induced losses by the end of the year, and it is doing so faster than any other major world economy. The recent strong rally in equity and property prices will also make policymakers think twice about large-scale stimulus which may disproportionately benefit the financial assets market, leading to a wider gap between the real economy and capital markets.

A slow and targeted implementation of policy easing is more likely, and consistent with recent signals from the People’s Bank of China and the Politburo. This should allow year-on-year GDP growth to reach 5%–6% in the second half, with growth at 2.3% for the whole of 2020.

最近,新冠疫情肆虐全球,而中国与美国的关系几乎降至冰点,逆全球化严重。但一些学者仍对中美关系前景持乐观态度。疫情对各个产业,个人,整个社会的影响都是不同的。同时,中国境内还发生了洪水等自然灾害。本文很好地阐述和描写了中国国内的状况,以及详细地将中美之间的关系进行了对比。为什么中国的经济可以从疫情中迅速反弹?整个世界,包括中国和美国,将来的经济计划和发展前景会是怎样的?本文为你解答了你想知道的各种问题。