This month’s report focus will be the review of the three most pressing questions facing the Chinese economy in the first half of 2012.

1. Chinese growth - is it sustainable in the midst of the global slowdown?

2. The Free fall of Chinese real estate and the likelihood of an economic hard-landing?

3. The People’s Bank of China easing the monetary environment and how much?

Can China maintain an economic growth rate above 8% for 2012? Most likely, no.

China's leadership is targeting growth of less than 8 per cent in 2012 according to senior government researcher Lin Zhaomu, reported Reuters on Sunday 8 January. Lin is a researcher affiliated with China's economic planning agency and the author of key economic documents for the Chinese leadership. Lin wrote that the 2012 target fell between 7 and 8 percent and had been adjusted to help Beijing deliver its plan for average GDP growth of 7 percent for 2011-2015.

While the government adjusts its expectation for economic growth, the market expects the Chinese economy, along with rest of Asia except Japan, to bottom out by the end of the first quarter.

The outlook for Asia, excluding Japan, has been improving recently as inflation retreated from its peak and the growth, including the United States economy, showed clearer signs of picking up, said Robert Prior-Wandesforde, Director of non-Japan Asia Economics at Credit Suisse.

"That is more constructive than we have been for the last 12 to 18 months," Xinhua reported on Saturday 7 January. Prior-Wandesforde said that the bank's central forecast for the euro zone is that there won't be a catastrophe in Europe over the next 12 months. He said inflation in Asia will fall quite heavily over the next few months as commodities prices soften, allowing more room for policy makers to focus on growth.

Nevertheless, Beijing will have to continue battling against the imbalances that have been formed over the past three years of expansionary fiscal policies.

China "overstretched itself a bit" in the past three years, said Dong Tao, Managing Director for non-Japan Asia Economics at Credit Suisse Hong Kong, adding that it would take a few years to correct the imbalances.

Tao said he expected China's economy to have a slowdown over the medium term with annual growth of 7 to9 percent. It is expected to grow by 8 percent in 2013, as no super factors like the WTO accession or the housing boom that has driven the China's economy in the recent years are emerging.

Tao cited challenges for China such as the banking sector failing its role as the financial intermediary. Most of the capital in banks is either locked or slowed down in terms of its velocity due to factors such as reserve requirements, local government debts, or trust funds, as well as State- owned enterprises. Furthermore, the real property sector, informal lending and local government debts were among the risk factors Tao identified.

Tao said he expected the Chinese yuan to manage an appreciation of 3-4 percentage points against the United States dollar "regardless of where the fundamentals are."

"This is an election year, and China does not want to engage in a trade war. The lawmakers on Capitol Hill have no clue what the real exchange rate is about," Tao said.

In the meantime, the wages of workers at the lower end of the pay scale will continue to rise, as a policy pillar to drive domestic consumption.

While China’s housing prices fall, will the country face a hard-landing?

China's housing prices are expected to fall by 15-20 percent in 2012 according to Tao at Credit Suisse. China’s stimulus package introduced in response to the 2008 global economic crisis has financed a large proportion of housing projects around the country. As property prices fall, developers will find it difficult to recoup their investment and start to default on their loans. Subsequently, local governments and state-owned banks will have to write down these loans as “non-performing.”

The worsening economic downturn, combined with Beijing’s firm stance on lowering property prices has triggered deep price discounts in tier one and tier two cities since October of 2011 and this process will quickly spread to other cities in China.

Mounting credit risks in China could strain its financial system in the years ahead. Not just falling property prices and rising non-performing loans, but also a growing number of Chinese corporate bond default has the potential to increase the likelihood of a hard landing.

“Defaults will be increasingly frequent because so much was borrowed over the past few years that has to be paid back now,” said Wang Jing, Head of Fixed-income Research with Jinyuan Securities.

There was big turbulence during the first week of January as two major Chinese companies were reported to experience difficulty repaying their debts. This underscored the increasing complexity of the Chinese economy and the new dangers that this entails.

Angang, one of China’s largest producers of steel, had been due to repay an AAA-rated CNY 5 bn (USD 793m) three-year note by 4 January. At 10:41 am that day, the China Government Securities Depository Trust & Clearing Co. announced it “had not received sufficient funds from the issuer.” By 4:10 pm, however, it posted a new notice, saying the debt had been paid according to a Financial Times report.

An unnamed Angang official told Chinese media that it had been a simple misunderstanding with the clearing company. Angang’s profits plunged 91 percent year on year in the first three quarters of 2011 as steel prices weakened, but there is no questioning its deep pockets – the listed company’s parent is a state-owned enterprise.

Angang’s case may have been simple miscalculation but another large case of bond default occurred shortly thereafter. Beijing DG Telecommunications Equipment Co, a manufacturer of wireless systems, said it had applied to its bond guarantor to cover debts that it could not pay.

Beijing DG Telecommunications had borrowed CNY 44m in 2010 as one of 13 small and medium-sized companies whose debt issues were combined together into a single bond – an innovation that regulators hoped would divide up risks for creditors and thereby make it easier for companies to obtain direct financing, according to Financial Times.

China’s corporate bond market has expanded dramatically in recent years. Debt issuance by mainland companies reached CNY 2.58 t last year, 52 percent more than in 2010, according to Thomson Reuters data.

The biggest default risks, however, are still concentrated in bank loans, as that was the form of financing mainly used to pay for China’s massive stimulus programme during the global financial crisis. Local governments owed CNY 10.7 t by the end of 2010, and 53 percent of that is coming due by the end of 2013, according to the national auditor.

How much will People’s Bank of China ease monetary policy?

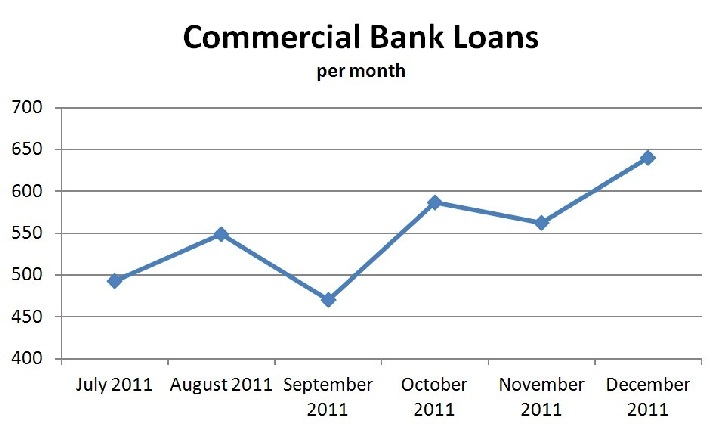

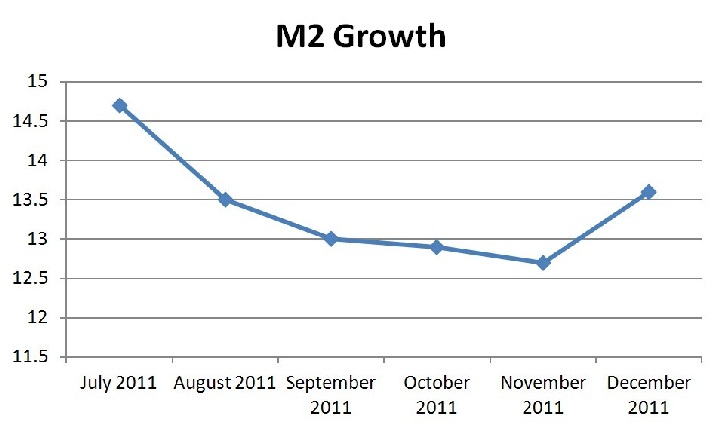

China’s lending and money supply growth exceeded economists’ estimates in December, signalling monetary conditions may be easing after regulators reduced banks’ reserve requirements for the first time since 2008, according to Bloomberg.

New loans totalled CNY 640.5 bn (USD101 bn) for the month, exceeding the estimates of all 18 economists surveyed by Bloomberg. M2, a measure of money supply, rose 13.6 percent, compared with the 12.9 percent median of 18 economists’ estimates.

Speaking at a financial planning conference on Sunday 8 January, Premier Wen Jiabao said China's financial industries are sound but still face risks. He also pledged to press ahead with reforms aimed at giving market forces more influence over lending but no details were announced following the two-day meeting, held to make plans for the industry over the next five years, according to AP.

Speaking at a financial planning conference on Sunday 8 January, Premier Wen Jiabao said China's financial industries are sound but still face risks. He also pledged to press ahead with reforms aimed at giving market forces more influence over lending but no details were announced following the two-day meeting, held to make plans for the industry over the next five years, according to AP.