The Chinese economy is slowing down. According to preliminary data released by the National Statistics Bureau, the GDP growth for the whole of 2011 was 9.2%, while growth in the fourth quarter was 8.9%, a decrease from the 9.1% growth recorded in the third quarter. The growth rate of fixed asset investment and industrial added value generally displayed deceleration over for the past several months, and the purchasing managers’ index (PMI) dipped to 49 in November, below 50 for the first time since March 2009.

However, with the inflation concern easing, recent messages sent by the central government show that a shift of focus for Chinese economic policies has been taking place. On 5 December, the People’s Bank of China (PBoC) lowered the required reserve ratio (RRR) by 50 bps, the first cut since 25 December 2008. During December 12th – 14th, the central government held its annual Central Economic Work Conference (CEWC), on which ‘stability’ was emphasized as the key word for policymaking for 2012, and ‘to maintain growth’ was placed ahead of ‘to control inflation’ on the work list. While the Conference mentioned that China will continue to implement a ‘proactive fiscal and prudent monetary policy’, we believe that the growth of new lending and M2 in 2012 will rise from the current low level to maintain a stable economic growth.

Market Performance

During the fourth quarter, 14 out of the 15 major cities recorded growth of office rent, with Hangzhou the only exception due to the large volume of new supply of low priced projects in the emerging submarket. However, impacted by factors such as global economic uncertainties and strong rental growth in previous quarters, leasing activity was observed slowing down in Beijing, Shanghai and Guangzhou, together with decelerating rental increases. Meantime, most of the tier-2 markets registered rental growth below 3%.

The prime retail property sector remained buoyant. Despite the fact that the average rents of some cities decreased due to delivery of new projects in rapidly growing new submarkets, most cities saw retail rents steadily trending upward. International fast fashion brands such as Zara, H&M, and Uniqlo have not only continued to expand in first tier cities, but also have grown their store network actively in second tier cities such as Chengdu, Chongqing, Wuhan and Hangzhou. Solid fundamentals and promising prospects for the retail property market have been attracting investor interest. Within the period under review, Mapletree’s first VivoCity in China opened in Xi’an.

Lasting home purchase restrictions started to show their influence on property prices. During this quarter, a decrease in the average luxury apartment price was seen in 11 of the 15 major cities, 8 more than the number for the third quarter. Turning to the logistics sector, we observed sustained strong demand this quarter, with prime warehouse space particularly undersupplied in Shanghai and Guangzhou. Logistics rents witnessed widespread growth this quarter, with no single city recording a negative change.

NORTH CHINA

Backed by limited supply and sustained demand, especially from the expansion of domestic companies, office rents in all five cities of north China recorded increases during the fourth quarter. Growth in Beijing and Dalian was particularly strong at 6.8% and 5.8% respectively, while Qingdao, Tianjin and Shenyang saw q-o-q rental increase of 0.5%, 1% and 2.2%. In the meantime, vacancy rates further decreased in the five markets, with Beijing hitting a historical low of 6.3%.

The impact of government regulations on the residential market has been further witnessed. During this quarter, price trends of luxury apartments in the five cities varied, with a 0.1% and 1.3% drop in Beijing and Qingdao, a slight increase of 1.7% and 0.2% in Tianjin and Shenyang, and no change in Dalian. For the leasing market, rental growth for luxury apartments was registered in all markets except in Dalian.

Within the period under review, prime retail rents in Qingdao and Shenyang saw marginal growth driven by steady demand, while rents in Beijing and Tianjin declined by 1.7% and 2.7% respectively due to the impact of new launches.

The rapidly developing e-commerce sector has been constantly generating new demand for logistics facilities. But, new logistics space has been undersupplied recently, and newly completed projects have generally been fully committed in the pre-leasing stage. During the fourth quarter of 2011, logistics rents in all five cities of north China showed q-o-q increases from 0.4% to 5%.

Tianjin

The Tianjin prime office market remained stable in the fourth quarter. No new projects were completed, and some buildings with a high vacancy in earlier periods showed notable improvement in absorption. Therefore, the average vacancy dropped by 2.8 percentage points over the period to 20.3%, and the average asking rent rose by 1% to CNY 119.8 sqm per month.

Nevertheless, more than 10 new office projects are in the pipeline for 2012, which will inevitably push up the vacancy rate in future quarters.

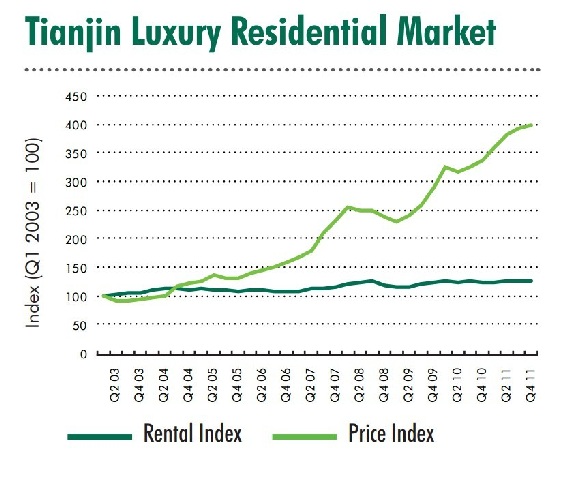

With curbing measures including home purchase restrictions in effect, the Tianjin residential market saw a decline in sales volume for the luxury residential market in the fourth quarter. Asking prices for the majority of projects remained flat, while the launch of high-quality new projects such as Tianjin Metropolis has driven the average luxury apartment price up by 1.7% q-o-q to CNY 21,419 sqm.

During the same period, the luxury residential leasing market remained stable, with average apartment rent increasing slightly by 0.3% to CNY 40.6 sqm per month.

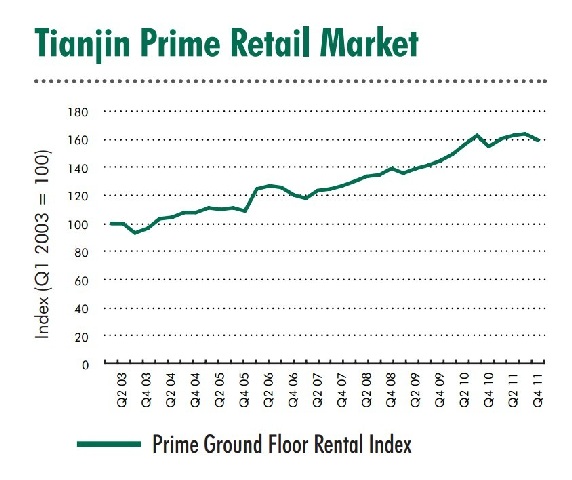

In the fourth quarter of 2011, the 80,000-sqm Tianjin Pengxin Aqua City opened with a high occupancy rate of 95%. The average vacancy rate dropped by 0.5% to 10.9%. Because of the relatively low pricing of Aqua City (not being in the core submarket) and the fairly high availability contributed by both existing and pipeline projects, this quarter saw average ground floor rents for prime retail properties decrease by 2.5% to CNY 21.4 sqm per day. Parkson Retail Group acquired the 45,022-sm Tianjin Building to open its second store in the city. A number of new projects are expected to open in 2012 which will bring heavy leasing pressure to the market.

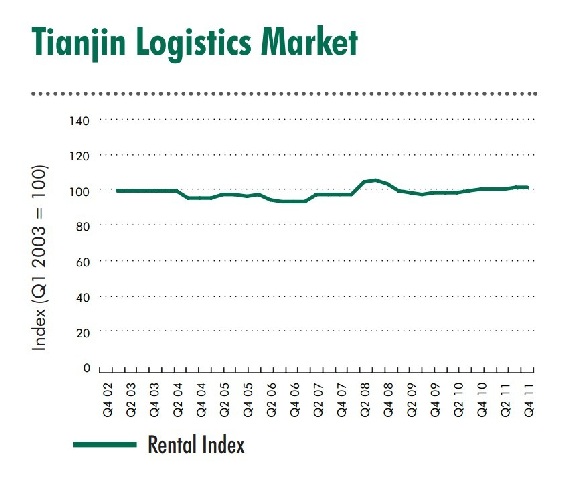

The Tianjin industrial property market demonstrated continued steady growth during the past quarter. The average rent of logistics facilities improved by 0.4% q-o-q to CNY 26.9 sqm per month, while the average industrial land price increased by 0.1% to CNY 451.9 sqm.

Tianjin local government is working actively to upgrade the local economic structure, including promoting the growth of the financial sector and headquarters economy, as well as developing more hi-tech industrial parks in the city. It is expected that both industrial rent and land prices will continue to rise in the future.

The prime retail property sector remained buoyant. Despite the fact that the average rents of some cities decreased due to delivery of new projects in rapidly growing new submarkets, most cities saw retail rents steadily trending upward. International fast fashion brands such as Zara, H&M, and Uniqlo have not only continued to expand in first tier cities, but also have grown their store network actively in second tier cities such as Chengdu, Chongqing, Wuhan and Hangzhou. Solid fundamentals and promising prospects for the retail property market have been attracting investor interest. Within the period under review, Mapletree’s first VivoCity in China opened in Xi’an.

The prime retail property sector remained buoyant. Despite the fact that the average rents of some cities decreased due to delivery of new projects in rapidly growing new submarkets, most cities saw retail rents steadily trending upward. International fast fashion brands such as Zara, H&M, and Uniqlo have not only continued to expand in first tier cities, but also have grown their store network actively in second tier cities such as Chengdu, Chongqing, Wuhan and Hangzhou. Solid fundamentals and promising prospects for the retail property market have been attracting investor interest. Within the period under review, Mapletree’s first VivoCity in China opened in Xi’an.