China has achieved a phenomenal increase in its GDP, from less than US$400 billion in 1990 to over US$7 trillion in 2011, meanwhile China’s foreign direct investment has also had a significant growth in the same period. Since the launch of the pilot scheme for RMB trade settlement in year 2009 and the RMB outbound direct investment scheme introduced in January 2011, RMB has become more widely used in trade and investment activities. Followed by rules respectively promulgated by the Ministry of Commerce (the “MOFCOM”) and the People’s Bank of China (the “PBoC”) on October 12, 2011 and October 13, 2011, foreign direct investment into China can also be made in RMB under said administrative rules. The building-up regulatory scheme and internationalisation of RMB make it possible for the issuers to successfully launch their RMB Bonds projects in Hong Kong, legally invest into the Mainland in RMB upon approval, and then repatriate the RMB funds, in the form of dividend, principals, interest, etc., in the future.

Qualified to Issue Bonds in RMB

The issuer base was expanded from Mainland

2-based Financial Institutions at the start, to Hong Kong-based companies and Multi-National Corporations (“MNCs”), and further to Mainland-based companies like BaoSteel this year

• Mainland-based Financial Institutions

On January 14 2007, PBOC promulgated its third notice of year 2007, in which the central bank of China pointed out that the financial institutions established in the Mainland could issue RMB-denominated bonds in Hong Kong upon approval. Following said notice, on June 8 2007, PBoC and the National Reform and Development Commission (the “NDRC”) jointly issued Provisional Measures on the Administration of Financial Institutions in Mainland Issuing RMB Denominated Bonds in the Hong Kong S.A.R. (the “Financial Institution Measures”), which opened a new financing channel for Mainland commercial banks and policy banks. The issuance of Dim-Sum Bonds by Mainland-based Financial Institutions is subject to the approval of PBoC and NDRC. Three weeks later, China Development Bank successfully launched Five Billion Yuan RMB-denominated bonds in Hong Kong.

• Hong Kong based Companies and MNCs

It was not clear who could be entitled to issue Dim-Sum Bonds other than Mainland-based Financial Institutions until the Hong Kong Monetary Authority publicised the Elucidation of Supervisory Principles and Operational Arrangements Regarding RMB Business in Hong Kong (the “Elucidation”) on February 10 2010. The Elucidation clarifies that the range of eligible issuers, issue arrangements and target investors can be determined in accordance with the applicable regulations and market conditions in Hong Kong. However, bonds issued by Mainland entities will continue to be governed by the relevant regulations and requirements in the Mainland. Since then, the Hong Kong based Companies and MNCs have become the active players in Dim-Sum Bonds market. McDonald, Tesco, Ford, Alstom and other MNCs who have extensive business in the Mainland set foot in Dim-Sum Bonds one after another.

• Mainland-based Non-Financial Enterprises

On November 25, 2011, Baosteel successfully issued 3.6 billion Yuan RMB-denominated bonds in Hong Kong, which is the first Dim-Sum Bonds issued by a Mainland-based non-financial enterprise. The issuance obtained a case-by-case approval from NDRC in October this year.

On May 2 2012, NDRC issued a Circular regarding Non-Financial Enterprises from the Mainland issuing RMB-denominated Bonds in Hong Kong (the “NDRC Circular 1162”) providing a legal basis for the issuance of Dim-Sum Bonds by Mainland-based non-financial Enterprises by specifying the qualified issuer, approval mechanism for the issuance of Dim-Sum Bonds and registration procedures regarding the cross-border transfer of RMB funds. NDRC and its provincial lever counterpart are entitled to approve the proposed transactions.

• Choose the Issuer

After the promulgation of NDRC Circular 1162, both onshore entity and offshore entity are eligible to issue Dim-Sum Bonds, provided certain requirements are duly satisfied in accordance with the applicable laws and regulations in which the issuer is incorporated, as well as the applicable laws and regulations of Hong Kong. To those MNCs who have a business presence in Mainland China, they could use its onshore subsidiary or the offshore entity, by themselves, or its offshore subsidiary, as the issuer. However, we are of the view that at the current stage, choosing an offshore entity as the issuer would be a better option for MNCs, due to the following reasons:

o Time-consuming NDRC’s Approval

According to NDRC Circular 1162, Mainland-based issuer3 shall submit the application and supporting documents for the issuance of offshore RMB bonds before NDRC or its provincial level counterpart. The application and supporting documents shall include the application report, board resolution (or other document with the same legal effect) on consent to the issuance of offshore RMB bonds, proposed scale of issuance, term and usage of raised funds, issuance plan, latest 3 years financial report and audit report, legal opinion, business license and other documents or materials required by NDRC.

Upon examination, NDRC and its local counterpart will issue its decision within sixty working days. The bond market is complex and inconstant and the sixty working days approval period may cause the issuer to miss the best window period. Therefore, additional efforts may be taken to shorten the approval period; however, it is out of the issuer’s control.

o Limitation on Use of the Proceeds

NDRC Circular 1162 indicates that the raised funds shall be mainly used for fixed asset investment projects, which may prevent the service providers who have limited fixed asset investment or onshore entities seeking for operational capital from obtaining approval from NDRC.

Besides, currently, most onshore issuers are state-owned entities managed by the central government and their offshore RMB issuance projects in Hong Kong are strongly encouraged by the central government. We are not sure of NDRC’s attitude on the issuance application made by Foreign Invested Entities (the “FIE”). It seems further observation will be taken for the clarification of the detailed requirement and approval procedures.

Use of the RMB Proceeds

The State Administration of Foreign Exchange (the “SAFE”) circulated Circular on Issues concerning Regulation of Operation of Cross-Border RMB Capital Account (the “SAFE Circular 38”) on April 7 2011 to officially regulate the foreign exchange registration procedure of the RMB funds in foreign direct investment and foreign debt sections. On October 12 MOFCOM promulgated the Circular on Issues Concerning Director Investment with Cross-border RMB (“MOFCOM Circular 889”) clarified the remittance and use of offshore RMB funds, including the RMB proceeds obtained through offshore RMB-denominated bonds issuance as direct investment by foreign investors. One day later, PBoC released Measures for the Administration of RMB Settlement Business for Foreign Direct Investment (the “PBoC Measures 145”) to rule bank account management and currency settlement issue for cross-border RMB.

The aforementioned rules respectively issued by SAFE, MOFCOM and PBoC constitute the framework for use of RMB proceeds in the Mainland, which end up PBoC’s case-by-case approval for RMB registered capital injection or shareholder loan registration and provide a transparently administrative formality for use of offshore RMB funds. According to these rules, the RMB proceeds could be used in the form of registered capital and/or foreign debt upon getting approval or registration before competent counterpart of MOFCOM and/or SAFE.

• Registered Capital

o Resource of offshore RMB

- Obtained through cross-border trading;

- Obtained through dividend distribution, equity transfer, capital reduction, liquidation and early returns of investment; and

- Other offshore lawful channels, such as offshore RMB-denominated bonds issuance (i.e. Dim-Sum Bonds), offshore RMB-denominated shares issuance, etc.

The foreign investors have to provide evidence of legal source of RMB funds for MOFCOM’s review.

o Approval Authority

The provincial level counterpart of MOFCOM are the approval authority; however, the following projects will trigger MOFCOM’s final opinion:

- For foreign invested entities (the “FIEs”) whose registered capital is more than RMB 300 million;

- For FIEs whose business scope covers financing guarantees, financial leasing, small-amount loans, auctions, etc.;

- For foreign invested holding companies, foreign invested venture capital firms or foreign invested private equity firms; and

- For FIEs investing in an industry subject to macro-economic planning by the State, e.g. cement, iron and steel, electrolysed aluminium, ship-building, etc.

MOFCOM shall complete the examination and issue its opinion within five working days upon receiving the Status Form regarding Cross-border RMB Foreign Direct Investment submitted by its provincial level counterparts. We are of the view that MOFCOM approval should not be deemed as a legal obstacle but a prudent examination regarding sensitive industries.

o Prohibited Usage

The offshore RMB funded registered capital cannot be used to invest in the stocks, financial derivations or provide entrustment loans to other entities.

o Repatriation

The RMB proceeds could be repatriated by ways of dividend distribution, equity transfer, capital reduction, liquidation, early returns of investment, etc as per agreed by the shareholders or directors or MOFCOM’s approval.

• Foreign Debt

The RMB proceeds can also be used in the form of foreign debt for financing the business of FIEs. Currently, the FIEs could borrow offshore RMB through issuance of Dim-Sum Bonds or from its parent company or affiliate, who could call funds through issuance of Dim-Sum Bonds as well. The RMB proceeds could be repatriated by ways of principal return and interest payment upon duly registration before SAFE.

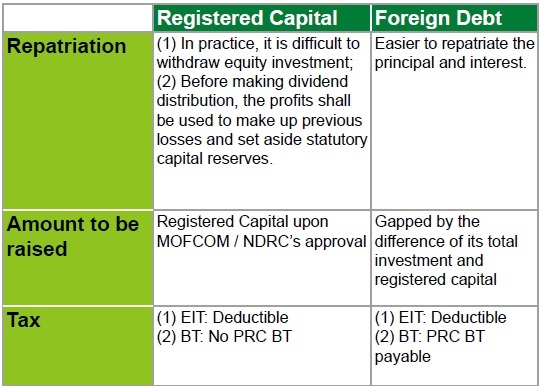

• Registered Capital vs. Foreign Debt

Comparing the two methods of using RMB funds from the said aspects, it seems lending foreign debt to FIEs, which only triggers SAFE foreign debt registration, is more flexible for the repatriation of the RMB funds. From a tax-saving perspective, using the RMB proceeds to contribute to the subscribed registered capital may be more tax-saving, since the repatriation of dividend and injected registered capital will not be subject to the PRC business tax. Each option has its pros and cons, the issuer could solely adopt one option or use both options. Therefore, it is highly recommended to scheme the method(s) based on the forecast and analysis on the demand of cash and profit margin before the issuance of bonds.

Garrigues’ Comments

It is undoubted that Hong Kong will continue to be the biggest offshore RMB hub. Meanwhile, other international financial centres, such as London and Singapore, are eager to expand their market share of RMB trading. Recently, HSBC has successfully raised RMB funds in London, which is the first RMB-denominated bonds issued in London. The expansion of RMB trading markets and competition among the financial centres will definitely benefit the issuers via providing more professional financing services and lower financial cost. Moreover, the stable growth of China’s economy and the sustainable internationalisation of RMB will ensure the abundant demand and supply of RMB funds. We’re seeing a wider range of business runners from a growing number of jurisdictions who are interested in raising funds through offshore RMB bonds to finance their expanding business.

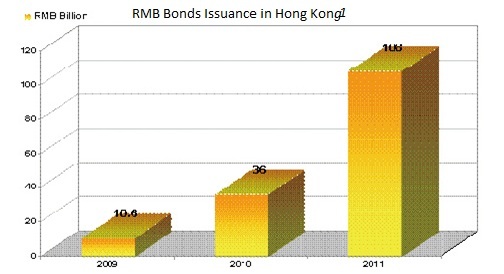

1Resource: Hong Kong Monetary Authority

2For the purpose of this article, the PRC or the Mainland excludes Hong Kong S.A.R., Macau S.A.R. and Taiwan Region.

3The Mainland-based issuer discussed under this section excludes Mainland-based financial institution. The approval procedure for offshore

RMB bonds issuance by Mainland-based financial institution are governed by Financial Institution Measures.