Q3 2012 was a quiet period in China in terms of completed transactions, although investors nevertheless retained a strong appetite for well-located, high quality commercial assets. Foreign groups had numerous transactions in the pipeline but it remained very complex for overseas buyers to complete deals in China given the lack of quality stock, difficulty in establishing an appropriate ownership structure and often lengthy period it takes to finalise agreements.

Buyers continued to seek greater exposure to sectors and assets tied to the domestic Chinese market as the government places greater emphasis on stimulating domestic consumption. Retail assets remain highly sought after with most overseas buyers seeking value added or opportunistic deals. However, there is very little quality product currently available for sale. Industrial and logistics properties are the subject of strong interest thanks to rising demand for quality facilities as the domestic retail market expands. Opportunities in this sector are also hard to come by, however, and it is challenging to locate good quality large assets. Business parks are also attracting increased attention from investors amid rising occupier demand for such accommodation from big name tenants seeking to escape high rental prices in cities such as Beijing and Shanghai.

The main focus of attention remains on the office sector where demand for high quality, well located assets with a good tenant profiles remains firm in tier I and leading tier II cities. In the residential market conditions are still challenging but the period saw greater optimism amongst investors that there could shortly be some relaxation of the severe cooling measures currently implemented on sales in this sector.

Banks remained cautious towards providing financing for real estate during the period and funding continued to be expensive and difficult to obtain. The majority of domestic developers were not actively looking to acquire new land, preferring instead to focus on completing existing developments and utilising their existing land banks.

The bulk of deals continue to be completed by domestic groups including State Owned Enterprises, private buyers and domestic RMB funds. Insurance companies are also expected to become more active in the market going forward following the China Insurance Regulatory Commission’s (CIRC) recent move to relax its restrictions on permitted investments, enabling insurance firms to invest up to 15% of their total assets in non-self-use real estate.

The outlook remains a relatively positive subject to any dramatic negative developments in the Eurozone. Whilst there is much talk about weaker growth in the domestic economy, there are no signs of a slowdown in investment in the real estate sector. Although many foreign buyers have taken a more conservative view on pricing and a price gap is beginning to emerge between buyers and sellers, domestic groups are less sensitive as they are generally acquiring more for their own requirements and self-use.

.jpg)

Net absorption in Beijing declined significantly to 36,200 sq m as market sentiment weakened despite demand continuing to outstrip supply. Vacancy declined marginally to 3.8% and rental growth slowed further to just 0.5% q-o-q. Corporations generally took longer to make leasing decisions but those in the automotive and pharmaceuticals sectors remained active. The lack of office space continues to inhibit major transactions alongside the softening demand.

Shanghai witnessed an active period as the completion of seven new office buildings in core submarkets resulted in a five-fold increase in net absorption to just under 185,800 sq m. The addition of the new stock also resulted in a slight rise in vacancy from 6.7% to 8.0%. Grade A rentals in core submarkets fell by 1.7% q-o-q, but decentralised locations registered growth. A number of multinational companies postponed expansionary moves amid the ongoing economic uncertainty. Rents are likely to be flat as the domestic economy slows but a significant fall is unlikely based on the moderate pipeline of new supply.

In Guangzhou, net absorption weakened to 84,400 sq m as overall leasing demand continued to slow. However, small domestic financial companies, insurance firms and State Owned Enterprises still committed to space for expansion or relocation. Space in existing buildings continued to be filled, driving down vacancy by 136 bps to 11.9%. Grade A rents increased by 0.3% q-o-q but may come under slight downward pressure as new projects in the Pearl River New City offer lower rents to attract tenants.

Shenzhen recorded net absorption of just 16,200 sq m as overall market sentiment remained soft despite a small uptick in leasing demand from multinationals. The period saw some flight to quality activity by firms in the financial and electronics sectors and vacancy fell to 8.6%. Grade A rents rebounded from a 1.0% decline in Q2 2012 to a 4.0% increase in Q3 2012. There is a strong pipeline of new supply over the next two years but half of this has been earmarked for self-use and will therefore only exert a minimal impact on rents and vacancy.

Demand Drivers

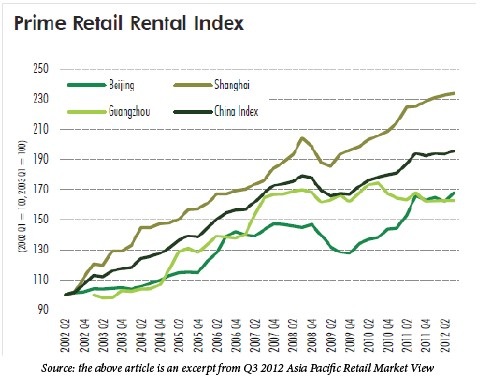

Leasing activity in China continued to slow in Q3 2012 as weaker domestic growth and the poor global economic environment forced retailers to turn more cautious. Although selected domestic and international retailers opened new stores in key markets, most groups have seen sales growth weaken in recent months and consequently have opted to be a lot more conservative in their expansion strategy. Retailers are now carefully identifying key markets and focusing on top requirements. However, despite the slowdown, demand for space in key areas continues to outweigh new supply.

Geographical Trends

International retailers continue to expand in Shanghai as new shopping centre supply comes on stream. Quality space in Beijing remains hard to come by, especially for the upper mid and top tier brands. Just one new high end mall in a core district is scheduled to be completed before the year end. Chengdu is an attractive market for luxury and accessible luxury retailers because of residents’ strong spending on consumer goods. However, options to expand in this market are limited for the moment as major new projects will not open until next year. Shenyang and Hangzhou are also on international retailers’ radar whilst a number of luxury brands have lodged enquiries for space in Hefei. Retailers are also launching flagship stores in Guangzhou.

Trends by Nationality of Company

Trends by Nationality of CompanyChinese retailers continue to expand – particularly in tier II, tier III and tier IV cities - but are focusing more on setting up profitable stores by securing favourable commercial terms as opposed to launching high profile shops in core locations. A number of domestic groups are expanding abroad to elevate the profile of their brand. International retailers continue to account for the bulk of demand in major cities in China and are expanding steadily. Among them, brands from the United States - generally those in the affordable mass market fashion sector – continue to dominate demand. Recent quarters have seen activity from Australian retailers, mostly in the affordable fashion accessories sector. Interest from Korean groups in the fashion and electronics sectors has also risen in recent months. There will be a particularly strong surge of new international entrants at the end of 2012 and beginning of 2013 when several new projects are completed in Shanghai.

Trends by Sector

Luxury brands had been considering expansion to new tier III locations but the slowdown has forced them to focus on existing markets. Fast fashion retailers continue to expand but at a slower pace than earlier in 2012. Nevertheless there is still plenty of room for growth in this segment from existing players and new entrants. Bridge brands and fashion retailers in the creative luxury sector are also expanding. In the F&B segment several strong regional players which have established themselves in tier I locations are now exploring entry in tier II cities. Children’s wear is seeing a lot of interest from international groups which are attracted by the fact that consumers in this segment are less price sensitive compared to other sectors. Other active sectors include cosmetics, although it remains complicated to register individual products for sale on the mainland which makes setting up a standalone store difficult.

Other Retail Trends

Groups from the United States and Europe remain very cautious in their home markets and are looking to Asia – and especially China - to deliver growth. However, many retailers – particularly in the fast fashion sector – have overbought stock in anticipation of strong growth and are now stuck with a huge amount of surplus inventory. Some groups are looking to redistribute this stock by selling it online. A number of retailers are increasing the amount of capital they spend on their shop fit-out and are pushing for longer lease terms to get the most out of their investment. Several groups have succeeded in securing four-year leases instead of the usual three. Retailers in the luxury goods and mid-range fashion sectors continue to move away from the franchising model as the market become more transparent and developed.

by CBRE