Recent Trends in Foreign Investment into China’s Property Market

By Sean Linkletter, Research Analyst, JLL

Investment into Chinese commercial real estate is a recent endeavor for foreign investors. Many of the current major foreign players did not even gain exposure to China until the mid-2000’s. Back then, almost all of foreign investment (inclusive of development) was concentrated in tier one cities, Beijing and Shanghai. However, the foreign investment market has grown dramatically, reaching a volume RMB 140 billion in 2014 and spread throughout multiple cities, tier one and tier two. The new market environment features new characteristics and a different set of players. It’s important to track investment trends as they truly shape the way cities develop.

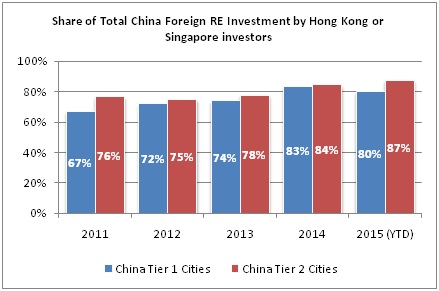

In China, most of the foreign capital into commercial real estate is sourced from either Hong Kong or Singapore. In 2015, Hong Kong and Singapore investment accounted for 80% of total foreign acquisitions in China tier one cities and 87% in tier two. This proportion has actually grown over time as current players increase their exposure and new players enter the Mainland market for the first time. For example, Hong Kong’s Link REIT entered the Mainland market just this year. Historically, Link REIT focused almost exclusively on managing a portfolio of real estate assets passed down from Hong Kong’s Housing Authority. The move should help the fund increase its brand awareness and asset diversity. They were quite active this year, acquiring Corporate Avenue 1 & 2, an office complex in Shanghai, as well as EC Mall in Beijing for a combined US$ 1.4 billion. Mapletree, a Singaporean investment company, acquired Sandhill Plaza in Shanghai for around US$ 300 million, their largest acquisition in Mainland China since 2011. Other active Hong Kong/Singapore players include Joy City, Yuexiu REIT and Gaw Capital.

Non-Asian investment accounts for a much smaller percentage of the total investment volume and is dominated by only a handful of players. The largest non-Asian player is Blackstone, an American investment fund, who acquired 16 projects in the past two years. Blackstone has a long history investing in China beginning in Shanghai back in 2008. Since then they have greatly increased their exposure, investing in office and retail in 15 cities.

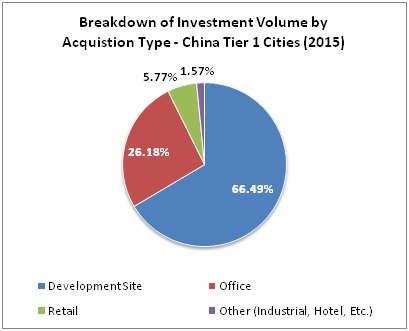

In terms of investment types, the majority of foreign investment in China is destined for development projects rather than acquisitions of existing property. This is especially true in tier two cities where more than 90% of foreign capital is used for development. Conversely, direct foreign investment into existing property is less common, only making up about 34% of the total volume in tier one and less than 10% in tier two. The large gap between tier one and tier two is mainly due to to tier one cities having a larger volume of tradable commercial stock. Grade A commercial properties are preferred by investment funds as they possess greater liquidity. In one study, JLL found that about 60% of international Grade A office space is located in tier one cities. Cities like Beijing and Shanghai possess strong service sectors where demand for high grade office space from MNC’s and domestic firms is robust.

Tier two has catching up to do. In 2013, the service sector only accounted for 53% of GDP in tier two cities, compared with over 64% in tier one (EIU). Retail, instead, takes up the majority of direct investment in tier two. This year, foreign direct investment volume into retail was RMB 4 billion compared with an office sector of just RMB 100 million.

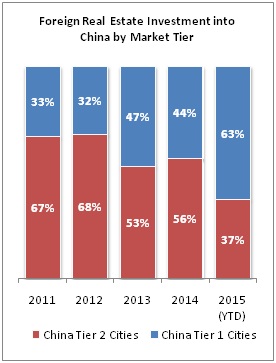

The share of total foreign investment volume into tier one cities has also increased over time. In 2015, over 63% of foreign investment is directed into tier one cities compared with only 33% in 2011. One possible explanations is that many foreign investment funds just recently began investing in China real estate and may not possess the necessary expertise to invest in markets outside of tier one. Among the top 50 foreign players in tier one, 10 invested for the first time within the last two years. The other explanation is that investing in tier two cities is more difficult than in the past. Many tier two cities now face oversupply where growth in rental values is actually negative. Tier two investment volume in development sites, which makes up an overwhelming majority of foreign investment in tier two, has declined almost 50% year-over-year. But even with weaker fundamentals, domestic sellers are largely unwilling to negotiate prices downwards. Their expectations of risk and return differ greatly from foreign funds, making it hard to get deals done.

To the contrary, investing in tier one may provide a security blanket for foreign investors. These markets face tight supply and stable rental growth. For example, office rents in Pudong increased over 8%, y-o-y, in the second quarter of this year. The service sector is expanding more quickly in tier one cities, Beijing’s emerging IT industry being a primary example.

While it’s likely many Chinese real estate markets face growing pains, the longer term prospects are still promising. China is unique in that its service sector is still largely underdeveloped and should see rapid growth over the next few decades. The office and retail sector should grow accordingly providing opportunities, long term, for investors who can navigate the market.

Sean Linkletter

Research Analyst, JLL

Graduated from Hopkins Nanjing Center and University of South Carolina

Dual degree in Investment Finance and Mandarin Chinese

--- END ---